National Atomic Company “Kazatomprom” JSC (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the fourth quarter and year ended 31 December 2023.

This update provides a summary of recent developments in the uranium and nuclear industries, as well as provisional information related to the Company’s key fourth quarter and 2023 operating and trading results, and 2024 non-financial guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

Nuclear energy became the most discussed topic at the UN Climate Change Conference, COP28, held in early December in Dubai. COP28 saw historical level of support for decarbonisation efforts and nuclear energy as a source of low-emission baseload energy in particular. More than 20 countries (with the exception of China and Russia) signed a declaration pledging to triple nuclear energy output by 2050. The declaration acknowledges that nuclear energy will be essential in reaching net-zero targets worldwide. Core aspects of the declaration also include intentions aimed at urging international financial institutions to encourage the inclusion of nuclear energy into their energy financing programs.

Furthermore, at COP28, UK, Canada, France, Japan, and the United States announced plans to raise $4.2 billion in government-led funding to create a safe and dependable worldwide nuclear energy supply chain. It is expected that over the next three years, these investments may increase the capacity for uranium enrichment and conversion, creating a robust global market infrastructure for uranium supplies, reducing the reliance on the Russian nuclear fuel cycle.

Finally, on the sidelines of COP28, an inaugural nuclear energy summit was announced to be held in Brussels in March 2024, where global leaders will gather to highlight the role of the nuclear energy in addressing challenges related to reduction of fossil fuels usage around the world, enhancement of energy security and boosting economic development.

Earlier in December 2023, the EU adopted the 12th sanctions package, which left Russian nuclear industry unaffected. Among the governments refusing to endorse the restrictions on the import of nuclear fuel from Russia are Slovakia and Hungary. Slovakia, along with Bulgaria, Czech Republic and Hungary, still procure nuclear fuel for its VVER reactors from Russia.

In late December, the U.S. House of Representatives passed H.R.1042, a legislative act prohibiting import of Russian enriched uranium products (EUP) starting from 2028. The ban, if passed, will start 90 days after enactment, with waivers available until 2028 in case of supply concerns among domestic nuclear reactors. The bipartisan bill is yet to be voted on by the U.S. Senate, however, several steps for enhancement of the U.S. domestic supply has already been made. Among them is President Biden’s ratification of the US$886 billion National Defense Authorization Act, which allocates funding and requires the National Nuclear Security Administration to submit a plan for the establishment of the domestic enrichment capacity.

Furthermore, in January 2024, the U.S. Department of Energy issued a request for proposals (RFP) for domestic enrichment services to help establish a reliable domestic supply of fuels using high-assay low-enriched uranium (HALEU) for advanced nuclear reactors. In total, President Biden’s Inflation Reduction Act will provide up to US$500 million for HALEU enrichment contracts selected through this RFP.

Among the recent instances of the overall trend towards Western enrichment capacity expansion are:

- commencement of enrichment operations at Centrus’s Ohio enrichment plant in October 2023 (900 kg of HALEU per year);

- Orano Board of Directors’ approval of the enrichment capacity extension at Georges Besse 2 by 30% (up to 2.5 million SWUs);

- Urenco’s approval of investments to expand enrichment capacity at its site in the Netherlands by 15% (additional capacity of around 750,000 SWU per year).

These expansion projects are expected to be completed in 2027–2028.

Beyond policy highlights, a number of new demand announcements took place during the fourth quarter:

- KHNP announced grid connection and first electricity generation at Shin Hanul 2. It became the fourth APR1400 reactor in operation. Meanwhile, Unit 5 of Hanbit NPP has been restarted after almost a year of maintenance outage.

- The world’s first 4th generation reactor has started its commercial operation in China. Shidaowan-1 is the first reactor of its type designed to use the fuel more efficiently, while also improving economics, safety, and environmental footprint of the power plant.

- Construction of Unit 1 of Xudapu Nuclear Power Plant commenced in November 2023. The new unit will employ a third-generation Chinese designed PWR reactor on top of the two existing VVER units under construction.

- China has also approved the construction of four new reactors: two-unit Jinqimen project, as well as the two additional units at Taipingling NPP.

- Belarusian-2, the second Rosatom-supplied VVER1200 in Ostrovets, Belarus, with a net capacity of 1.11 GWe has started commercial operation in November 2023.

- Rostekhnadzor, the Russian Federal Service for the Supervision of Environment, Technology and Nuclear Management, has issued the licenses to Rosatom for the construction of Units 7 and 8 at the Leningrad NPP.

- In December, Belgian government and Engie have finally signed the agreement to extend the operation of the Tihange 3 and Doel 4 reactors for up to ten years. Belgium is the first and so far the only European country to reverse a nuclear energy ban decision. The reactors will return to operation no earlier than November 2025.

- Turkish Nuclear Regulatory Authority issued a permit authorising the commissioning of Unit 1 at the Akkuyu NPP. Turkey’s first reactor with a 1.2 GWe capacity is expected to be operational in 2024.

- California’s Public Utilities Commission approved an extension for Units 1 and 2 at the Diablo Canyon NPP until 2030.

On the supply side, in November 2023, enCore Energy commenced uranium production at the South Texas Rosita project. Meanwhile, Australian Boss Energy has become a shareholder of enCore's Alta Mesa following the announcement of the acquisition of a 30% ownership stake. Alta Mesa has 3.41 million lbs U3O8 of measured and indicated, as well as 16.79 million lbs U3O8 of inferred resources. The production at Alta Mesa is expected to start in early 2024.

Energy Fuels has begun mining operations at three mines in Arizona and Utah. The company expects the annual production of 1.1 – 1.4 million lbs U3O8.

Boss Energy announced the commencement of mining activities at Honeymoon ISR project in October 2023, with the first well field being pre-conditioned in the lead-up to in-situ recovery, feeding the processing during the December of 2023. The mine is expected to restart in the first quarter of 2024, ramping up to 1.8 million lbs U3O8 in 2026, with a nominal annual capacity of 2.45 million lbs U3O8 for 10 plus years.

Paladin Energy’s Langer Heinrich mine is also expected to restart its production in the first quarter of 2024, after being placed into care and maintenance since 2018 due to the sustained low uranium price environment. The nominal production capacity of the mine is expected to be up to 6 million lbs U3O8 per annum with an estimated 17-year mine life.

In late 2023, the Ministry of Mines and Energy of Namibia has granted mining licenses to Deep Yellow for the Tumas project and Bannerman Energy for the Etango project.

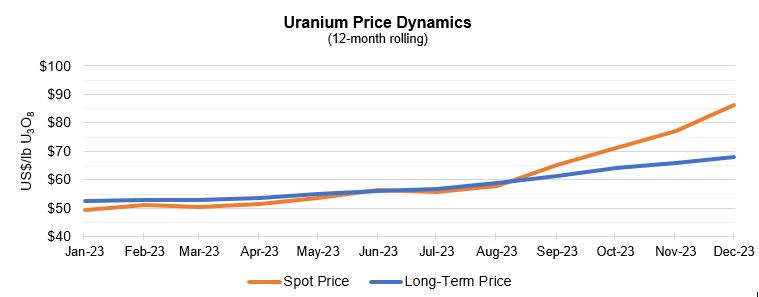

Market Pricing and Activity

* Average of the UxC and TradeTech reported prices

Throughout October, the spot market was volatile with prices falling below $70 per pound U3O8 in the beginning of the month. However, the price started a gradual rise again in the second half of the month due to increased demand. In November, the spot price continued to rise, surpassing the $80 per pound level. The spot price kept setting new records in December – for the first time in 16 years, the spot price exceeded $90 mark. As a result, the price rose by 32% to $91 per pound U3O8 during the fourth quarter.

As per the third-party market data, the spot market volumes transacted throughout 2023 were almost 20% lower than in 2022. A total of 42.8 million pounds U3O8 (~16,400 tU) were transacted at an average weekly spot price of US$60.53/lb U3O8 in 2023, compared to about 52 million pounds U3O8 (~20,000 tU) at an average weekly spot price of US$49.61/lb U3O8 in 2022.

In the term market, 2023 contracting activity was notably higher than in the previous year, with the third-party data indicating that contracted volumes totalled about 160 million pounds U3O8 (~61,500 tU) throughout 2023, compared to about 114 million pounds U3O8 (~43,800 tU) in 2022. The increase in term market activity resulted in an increase of the average long-term price indicator by US$16/lb U3O8 year-over-year, to US$68/lb U3O8 by the end of 2023 (reported on a monthly basis by third-party sources).

Company Developments

Credit Rating

On 19 January 2024, Fitch Ratings upgraded Kazatomprom’s credit rating from BBB- to BBB, Outlook – Stable. The main drivers for the upgrade were cited as follows: sustained low leverage, positive uranium price dynamics and tightness of the market, strong market position, availability of alternative transportation routes, and high-expected dividend payments. Fitch rates Kazatomprom on a standalone basis due to limited ties with the state represented by Samruk-Kazyna JSC, which owns 75% of the Company’s shares (according to Fitch’s rating criteria for government-related companies).

Fitch’s press release on Kazatomprom’s rating upgrade can be accessed at the following link: https://www.fitchratings.com/research/corporate-finance/fitch-upgrades-jsc-national-atomic-company-kazatomprom-to-bbb-outlook-stable-19-01-2024.

Sulphuric acid market

In January 2024, the Company unveiled anticipated revisions to its 2024 production plan, primarily driven by challenges associated with the availability of sulphuric acid, a crucial component in the ISR uranium mining method.

As reported by S&P Global Commodities Insights agency, sulphuric acid is among the most prevalent chemical commodities and finds applications across a diverse spectrum of industries. Approximately 60% of the world's sulphuric acid is utilised in the production of fertilisers. Consequently, the agricultural sector wields a substantial influence on the demand for sulphuric acid. This phenomenon extends to the domestic Kazakh sulphuric acid market, where the agricultural industry is regarded as a vital element in ensuring food security and, as such, is subject to substantial subsidies, further propelling the demand for fertiliser production.

Given the significant increase in the domestic consumption and the demand for sulphuric acid for fertiliser production over the past few years, a shortage of sulphuric acid has developed in the domestic market. Regional markets are also experiencing a deficit due to growing demand from agricultural sector and a combination of factors such as supply chain disruptions and geopolitical uncertainty. As a result, current demand affects both availability and pricing of sulphuric acid. As of 12 months 2023, Kazatomprom’s weighted average cost of sulphuric acid increased by 33.6% to KZT 40,445 per tonne from KZT 30,263 per tonne in 2022. The 2022 year-on-year increase was 33%.

Sulphuric acid is categorised as a Class 8 material owing to its toxic and corrosive attributes. This classification exerts a substantial impact on various aspects, including safety protocols, logistical operations, and the economically viable transportation methods for its import from international markets, particularly those situated beyond neighbouring countries.

Presently, the Company is actively pursuing alternative sources for sulphuric acid procurement. Looking ahead in the medium term, the deficit is expected to alleviate as a result of the potential increase in sulphuric acid supply from local non-ferrous metals mining and smelting operations. The Company also intends to enhance its in-house sulphuric acid production capacity by constructing a new plant.

Update on Taiqonyr Qyshqyl Zauyty LLP

In January 2024, as part of the restructuring process aimed at optimising ownership structure, Kazatomprom divested its 49% stake in the authorized capital of Taiqonyr Qyshqyl Zauyty LLP (“TQZ LLP”) to Kazatomprom-SaUran LLP. As a result, ownership of TQZ LLP is now split between Kazatomprom-SaUran LLP with a 75% share and RU-6 LLP with a 25% share, both of them being 100%-owned subsidiaries of Kazatomprom.

As previously disclosed, the construction of the TQZ LLP sulphuric acid plant serves as a strategic risk mitigation initiative aimed at ensuring self-reliant production capabilities. The plant is anticipated to have a nominal capacity of 800,000 tonnes of sulphuric acid annually. When combined with the existing in-house production capacities of SKZ-U LLP and SSAP LLP, totalling around 680,000 tonnes, Kazatomprom envisions a consolidated sulphuric acid production volume of approximately 1.5 million tonnes.

In January 2024, a significant step towards securing investment for the construction of a new sulphuric acid plant was achieved through the establishment of a strategic partnership with the renowned Italian firm, Ballestra S.p.A., and Kazatomprom’s Board of Directors made a decision to engage a local partner of Ballestra in Kazakhstan for this project. Under this partnership, Ballestra will assume responsibility for the project's design, equipment procurement, and provision of technical support. It is worth noting that Ballestra's technology has a well-documented history of successful implementation at the existing sulphuric acid plants, SKZ-U LLP and SSAP LLP.

Considering that sulphuric acid production is not Kazatomprom’s core business, the Company expects to decrease its indirect ownership in TQZ LLP via Kazatomprom’s fully-owned subsidiaries.

Transportation risk mitigation

Kazatomprom diligently tracks the evolving sanctions landscape concerning Russia and assesses their potential implications for uranium transit through Russian territory. As of now, there are no constraints impacting the Company's global product supply chain. Notably, Kazatomprom successfully executed its fourth-quarter shipments, experiencing no interruptions, logistical or insurance-related challenges.

The Company has effectively leveraged the Trans-Caspian International Transport Route (TITR) since 2018. In the entirety of 2023, 64% of all uranium shipments originating in Kazakhstan and destined for Western markets were efficiently transported via the TITR. The deviation from the initially projected 71% share of export shipments through the TITR in 2023 was primarily attributed to an unanticipated export delivery to France through the northern transport corridor during the fourth quarter of the same year. This resulted in a lower proportion of shipments via TITR. The breakdown and dynamics of transportation costs within the selling expenses will be disclosed in the Company’s FY2023 Operating and Financial Review.

2023 Mineral Resource and Ore Reserve Statements and Operating and Financial Review

An update of the Mineral Resource and Ore Reserve statements as of December 31, 2023, prepared by SRK Consulting, is expected to be disclosed on 15 March 2024, the same day with the Company’s FY2023 Operating and Financial Review.

Kazatomprom’s Fourth-Quarter and 2023 Operational Results1

|

|

Three months ended December 31 |

|

Year ended December 31 |

|

||

|

(tU as U3O8 unless noted) |

2023 |

2022 |

Change |

2023 |

2022 |

Change |

|

U3O8 Production volume (100% basis)2 |

5,795 |

5,780 |

0% |

21,112 |

21,227 |

-1% |

|

U3O8 Production volume (attributable basis)3 |

3,066 |

3,064 |

0% |

11,169 |

11,373 |

-2% |

|

Group U3O8 sales volume4 |

5,863 |

3,025 |

94% |

18,069 |

16,358 |

10% |

|

KAP U3O8 sales volume (incl. in Group)5 |

3,817 |

1,340 |

185% |

14,915 |

13,572 |

10% |

|

Group average realized price (USD/lb U3O8)6* |

68.41 |

47.51 |

44% |

55.06 |

43.46 |

27% |

|

KAP average realized price (USD/lb U3O8)7* |

64.07 |

48.61 |

32% |

52.06 |

42.51 |

22% |

|

Average month-end spot price (USD/lb U3O8)8* |

82.21 |

49.94 |

65% |

62.51 |

49.81 |

25% |

Kazatomprom 2023 production and sales results were within the guided ranges. Production volumes on both a 100% and attributable basis were slightly lower throughout 2023 compared to 2022, primarily due to an insignificant decrease in the production plan for 2023, compared to 2022.

Throughout 2023, both Group and KAP sales volumes were higher compared to 2022, primarily due to additional requests from customers to flex up their annual delivery quantities within the frame of existing contracts, as well as some new long-term contracts with the delivery in a prompt window during 2023. Sales volumes may vary substantially each quarter, and quarterly sales volumes vary year to year due to the timing of customer delivery requests during the year, and physical delivery activity.

Average realized prices for both the fourth quarter and throughout 2023 were higher compared to the same periods in 2022 due to a higher uranium spot price. The Company’s current overall contract portfolio pricing correlates to the uranium spot prices, however deliveries under some long-term contracts in 2023 incorporated a proportion of fixed pricing components, including price ceilings, that were negotiated during a comparatively lower price environment. As a result, growth of both the Group and KAP’s average realized prices in the fourth quarter was lower than the increases in the spot market price for uranium over the same intervals, however the year-on-year growth rates for all three indicators were at a similar level.

Kazatomprom’s 2024 Production and Sales Guidance

|

2024 |

2023 |

|

|

Production volume U3O8 (tU) (100% basis)1 |

21,000 – 22,500 |

20,500 – 21,500 |

|

Production volume U3O8 (tU) (attributable basis)2 |

10,900 – 11,900 |

10,600 – 11,200 |

|

Group U3O8 sales volume (tU) (consolidated)3 |

15,500 – 16,500 |

18,000 – 18,500 |

|

Incl. KAP U3O8 sales volume (incl. in Group) (tU)4 |

11,500 – 12,500 |

14,650 – 15,150 |

Kazatomprom’s 2024 uranium production volumes are expected to be in the range of 21,000 – 22,500 tonnes on a 100% basis and in the range of 10,900 – 11,900 tonnes on an attributable basis. Adjustments to the previously announced production intentions are due to challenges related to the availability of sulphuric acid and construction delays at the newly developed deposits, as highlighted in the Company’s announcement on 12 January 2024.

The Company anticipates that the production volume for the majority of its uranium mining operations will be approximately 20% below the levels stipulated in the Subsoil Use Agreements. Nonetheless, the Company projects a modest annual growth in production for the year 2024. The Company will use all reasonable efforts to ensure it complies with its production volume obligations under the Subsoil Use Agreements. Concurrently, entities engaged in mining operations at newly established deposits face the potential challenge of descending beneath the threshold of minus 20% (in relation to the stipulations of the Subsoil Use Agreements). This risk is primarily attributed to delays in the construction of surface facilities and infrastructure. These delays, in turn, are a consequence of the extended timelines required for the development and subsequent approval of project design documentation.

Kazatomprom is actively engaged in discussions with sulphuric acid manufacturers in the neighbouring countries to augment the supply volumes for 2024. The Company is committed to addressing this matter diligently and will keep stakeholders informed about the evolving situation regarding sulphuric acid availability and its potential influence on production metrics.

The Company remains committed to its market-centric strategy, creating long-term value for its shareholders. The Group sales volumes are expected at the range of 15,500 – 16,500 tU, which includes KAP sales of 11,500 – 12,500 tU. Decrease in 2024 sales volume guidance in comparison to 2023 at both the Group and KAP levels is due to higher sales of EUP to “Ulba-FA” LLP for subsequent production of fuel assemblies and aimed at ensuring sufficient level of inventories for the future periods.

Kazatomprom remains committed to its 2024 contractual obligations to all existing clients. The Company has a comfortable level of inventories to fulfil its existing contractual commitments in 2024 and will persist in ensuring the availability of essential inventory levels, thereby ensuring its capability to fulfil delivery commitments while optimising resource utilisation. Additionally, we usually reserve a segment of our annual production as uncommitted. This approach enables us to capitalize on emerging opportunities and adapt to fluctuations in the market landscape. This strategic approach enables the Company to mitigate risks effectively and uphold our contractual obligations to clients, even amidst production-related challenges.

If the limited access to sulphuric acid continues throughout the current year and the Company does not succeed in reducing the delay in the construction schedule at the newly developed deposits in 2024, this could unfavourably influence Kazatomprom’s production plans for 2025. Should there be any adjustments to the 2025 production plans, these are expected to be announced in the report of the Company’s financial results for the first half of 2024. However, a swift return to a 100% production volume level relative to Subsoil Use Agreements may be at risk.

Financial guidance for 2024 will be published in the Operating and Financial Review for 2023, expected to be released on 15 March 2024.

Conference Call Notification – FY2023 Operating and Financial Review (15 March 2024)

Kazatomprom expects to schedule a conference call to discuss the FY2023 financial results after they are released on Friday, 15 March 2024. Further details will be provided closer to the date of the event.

For further information, please contact:

Investor Relations Inquiries

Botagoz Muldagaliyeva, Director, Investor Relations

Tel: +7 7172 45 81 80/69

Email: ir@kazatomprom.kz

Public Relations and Media Inquiries

Askar Atagulin, Director, Public Relations

Tel: +7 7172 45 80 63

Email: pr@kazatomprom.kz

A copy of this announcement is available at www.kazatomprom.kz.

About Kazatomprom

Kazatomprom is the world's largest producer of uranium, with the Company’s attributable production representing approximately 22% of global primary uranium production in 2022. The Group benefits from the largest reserve base in the industry and operates, through its subsidiaries, JVs and Associates, 26 deposits grouped into 14 mining assets. All of the Company’s mining operations are located in Kazakhstan and extract uranium using ISR technology with a focus on maintaining industry-leading health, safety and environmental standards (ISO 45001 and ISO 14001 compliant).

Kazatomprom securities are listed on the London Stock Exchange, Astana International Exchange, and Kazakhstan Stock Exchange. As the national atomic company in the Republic of Kazakhstan, the Group's primary customers are operators of nuclear generation capacity, and the principal export markets for the Group's products are China, South and Eastern Asia, Europe and North America. The Group sells uranium and uranium products under long-term contracts, short-term contracts, towards the second shareholders of jointly owned subsidiaries, as well as in the spot market, directly from its headquarters in Astana, Kazakhstan, and through its Switzerland-based trading subsidiary, Trade House KazakAtom AG (THK).

For more information, please see the Company website www.kazatomprom.kz.

Forward-looking statements

All statements other than statements of historical fact included in this communication or document are forward-looking statements. Forward-looking statements give the Company’s current expectations and projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “target”, “believe”, “expect”, “aim”, “intend”, “may”, “anticipate”, “estimate”, “plan”, “project”, “will”, “can have”, “likely”, “should”, “would”, “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future.

THE INFORMATION WITH RESPECT TO ANY PROJECTIONS PRESENTED HEREIN IS BASED ON A NUMBER OF ASSUMPTIONS ABOUT FUTURE EVENTS AND IS SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTY AND OTHER CONTINGENCIES, NONE OF WHICH CAN BE PREDICTED WITH ANY CERTAINTY AND SOME OF WHICH ARE BEYOND THE CONTROL OF THE COMPANY. THERE CAN BE NO ASSURANCES THAT THE PROJECTIONS WILL BE REALISED, AND ACTUAL RESULTS MAY BE HIGHER OR LOWER THAN THOSE INDICATED. NONE OF THE COMPANY NOR ITS SHAREHOLDERS, DIRECTORS, OFFICERS, EMPLOYEES, ADVISORS OR AFFILIATES, OR ANY REPRESENTATIVES OR AFFILIATES OF THE FOREGOING, ASSUMES RESPONSIBILITY FOR THE ACCURACY OF THE PROJECTIONS PRESENTED HEREIN.

The information contained in this communication or document, including but not limited to forward-looking statements, applies only as of the date hereof and is not intended to give any assurances as to future results. The Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to such information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date hereof.