JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the second quarter and half-year ended 30 June 2020.

This update provides a summary of recent key developments in the uranium industry, provisional information related to the Company’s key second quarter and half-year operating and trading results, and reiterated 2020 guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

The COVID-19 pandemic, which took hold in earnest at the end of the first quarter of 2020, continued to spread throughout the second quarter with a significant impact on global economies. The slowdown in manufacturing and commercial activities has impacted the energy sector; along with oil and other fossil fuels, the electricity sector has seen a large fall in demand of approximately up to 20% in most countries. However, within the electricity sector, the impact on nuclear generation has been much less severe, reflecting the resiliency and base load nature of nuclear power plants on the grid.

In its 2020 Global Energy Review, the International Energy Agency estimated nuclear power generation could decline by up to 3% in 2020 (compared to 2019), with extended outages and potential schedule delays in new plant construction being the most likely impact of the COVID-19 lockdowns. These include the following announced reductions and delays:

- Swedish utility OKG announced a three-week extension of its planned third-quarter maintenance and refueling outage for the Oskarshamn-3 nuclear power plant, aiming to reduce the spread of COVID-19 amongst plant workers.

- In the US, DTE Energy of Detroit saw a COVID-19 outbreak in its workforce, resulting in an extended maintenance shutdown for the Fermi-2 nuclear power plant. Referred to by the company as a “safety stand-down”, the ongoing shutdown started 21 March and is the longest shutdown the plant has seen since 1993.

- Romania's Nuclearelectrica postponed a planned maintenance outage of Cernavoda-1 to ensure continuity of operation and production under measures in its Staff Protection Plan for COVID-19.

- Rosenergoatom of Russia is expecting a two-month delay in commissioning of the Leningrad II-2 nuclear reactor due to Russian government restrictions imposed to prevent the spread of COVID-19.

- In Ukraine, Energoatom temporarily suspended the operation of three of its 15 nuclear power units during parts of the second and third quarters, largely due to reduced electricity demand.

Additional construction delays are possible for projects in France, the United Kingdom and the United States, although most companies are continuing to assess the overall impact and duration of the crisis, prior to making any announcements.

In Japan and unrelated to the pandemic, Kyushu Electric Power Co. suspended the operation of a second reactor at its Sendai nuclear plant in order to meet strict new safety guidelines. The shut-down follows the suspension of generation at the complex’s other unit in March, with both reactors expected to return to service in 2021, once construction of the required antiterrorism facilities has been completed.

In the US, Entergy permanently shut down the Indian Point-2 reactor after nearly 46 years of generating safe, clean electricity. The decommissioning was part of a deal reached in 2017 between Entergy, the state of New York, and the environmental group, “Riverkeeper”.

French utility EDF permanently shut down Fessenheim-2 in eastern France. Fessenheim's two 880 MWe pressurized water reactors have been in operation for more than 40 years, but have now both been shuttered to meet requirements under France’s energy transition law, adopted in August 2015.

Nuclear utilities purchase fuel long before it is needed and the abovementioned demand side developments have generally had a limited impact on the near-term uranium market. In contrast, events impacting the supply side have already begun to impact the near- and medium-term market far more significantly.

The impact of COVID-19 on global primary uranium supply has already been seen in most mining jurisdictions. Driven by the need to keep employees safe and follow local health regulations, the temporary suspensions and production reductions announced by major uranium producers in Kazakhstan, Canada, Namibia and other locales in March and April, started to take effect during the second quarter, with some reductions carrying into the third quarter. Based on the latest annual production volume guidance updates, at the end of July, compared to volumes announced before COVID-19 pandemic, analysts are forecasting a reduction of more than 15 million pounds U3O8 (more than 10%) in 2020, pushing the supply-demand balance into a supply deficit and reducing inventories.

On the policy front, the US Administration announced in May that it would end sanction waivers for three Iranian projects – the redesign of the Arak heavy water reactor, the Russian supplies of uranium to fuel the Tehran Research Reactor, and Russian export of Iran’s scrap and spent fuel from the research reactor. Foreign companies involved in these projects were given 60 days to wind down activities. A 90-day extension was provided for the fourth waiver, covering ongoing international support to the Bushehr-1 nuclear power plant, in order to ensure safety of operations.

In other US developments, the US House of Representatives Committee on Appropriations (the “Committee”) directed the US Department of Energy (the “DoE”) to re-submit a plan for the proposed establishment of a uranium reserve, prior to the reserve being funded in the FY2021 Energy and Water Development and Related Agencies Appropriations Bill. The Committee determined that the DoE, acting on the recommendations of the US Nuclear Fuel Working Group (established following the Section 232 investigation completed in 2019), had not provided sufficient information about how it would implement the program. The Committee gave the DoE 180 days to resubmit a plan.

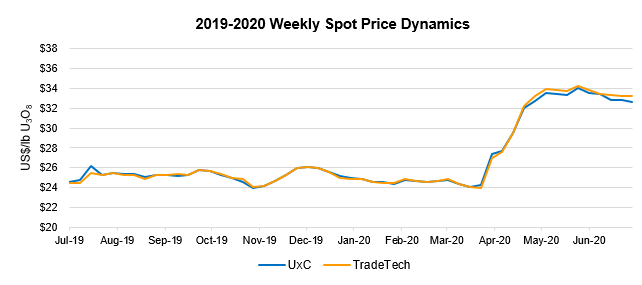

Spot Market

The volumes transacted in the spot market increased considerably in the second quarter, following announcements from several producers indicating the global pandemic would have an impact on primary supply in 2020. Over the quarter, the market saw a steep spot price increase from about US$27.50 at the beginning of April, to US$34.00 by the end of May. Utilities remained largely on the sidelines, their focus being on ensuring the safety and continuity of their operating environments amid COVID-19. Producers and intermediaries were therefore the primary buyers in the spot market throughout the quarter, replacing lost production volumes with tonnage from the spot market to backstop their delivery obligations.

According to third-party market data, spot volumes transacted over the second quarter of 2020 were nearly three times higher than the same period last year. A total of 27.3 million pounds U3O8 (10,500 tU) was transacted at an average weekly spot price of US$32.56 per pound (compared to 10.5 million pounds U3O8 (4,050 tU) at an average weekly spot price of US$24.88 per pound in the second quarter of 2019).

Long-term Market

In the term uranium market, third-party data indicated that contracted volumes amounted to nearly 3.5 million pounds U3O8 (1,350 tU) through the second quarter of 2020, compared to about 17.7 million pounds U3O8 (6,800 tU) in the second quarter of 2019. Although the term market saw a sharp drop in activity in the second quarter of 2020 compared to last year, the average long-term price increased by about US$3.00 per pound U3O8 to US$35.50 (reported only on a monthly basis by third-party sources).

Company Developments

COVID-19 Update

To reduce the risk of a COVID-19 outbreak at Kazatomprom’s operations and to follow all government restrictions and recommendations, the number of employees on mine sites was reduced for a four-month period, from April through July 2020. With carefully developed plans to ensure compliance with distancing and hygiene requirements during shift changes and day-to-day operations, the Company believes it can now safely begin to gradually bring staff back to the mine sites.

During the first half of August, the operations are expected to begin mobilizing employees, with COVID-19 testing for all workers returning to site. The sites are expected to be back to normal staff levels within two to three weeks. The ramp-up will be carried out following strict health and safety protocols to minimize the risk of a potential outbreak. However, production levels for the second half of the year are expected to be severely impacted by the four month shutdown.

Thanks in part to the timely pandemic response measures taken by Kazatomprom’s management in April, there have been no outbreaks at Kazatomprom’s sites, despite increasing cases across Kazakhstan and a number of cases among the off-site staff. The Company will continue to monitor the situation at the operations, as well as all regional COVID-19 developments and governmental directives, ensuring that any further recommended actions to reduce the impact of the pandemic are implemented without delay.

Shareholder structure

In early June, Joint-Stock Company “Sovereign Wealth Fund “Samruk-Kazyna”, Kazatomprom’s majority shareholder, placed an additional 6.28% of Kazatomprom’s shares for public sale on the Astana International Exchange and London Stock Exchange. Following the secondary placement, the Company’s public free-float is now 25%, as was planned under the Government Privatization Plan.

Kazatomprom’s 2020 Second Quarter Operational Results1

|

|

Three months ended June 30 |

|

Six months ended June 30 |

|

||

|

(tU as U3O8 unless noted) |

2020 |

2019 |

Change |

2020 |

2019 |

Change |

|

Production volume (100% basis)2 |

5,213 |

5,506 |

(5)% |

10,434 |

10,800 |

(3)% |

|

Production volume (attributable basis)3 |

2,809 |

3,163 |

(11)% |

5,790 |

6,226 |

(7)% |

|

Group sales volume4 |

2,466 |

3,780 |

(35)% |

4,220 |

5,425 |

(22)% |

|

KAP sales volume (incl. in Group)5 |

2,231 |

3,143 |

(29)% |

3,749 |

4,608 |

(19)% |

|

KAP average realized price (USD/lb U3O8)6* |

28.75 |

27.69 |

4% |

27.81 |

27.43 |

1% |

|

Average month-end spot price (USD/lb U3O8)7* |

33.33 |

24.62 |

35% |

29.46 |

26.01 |

13% |

1 All values are preliminary.

2 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it therefore disregards the fact that some portion of that production may be attributable to the Group’s joint venture partners or other third party shareholders. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, which corresponds only to the size of such interest; it therefore excludes the remaining portion attributable to the JV partners or other third party shareholders, except for production from JV “Inkai” LLP. The Company anticipates that the annual share of production in JV “Inkai” LLP in 2020 will be approximately 1,066 tU. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

4 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity).

5 KAP sales volume (incl. in Group): includes only the total external sales of KAP HQ and Trade House KazakAtom AG (THK). Intercompany transactions between KAP HQ and THK are not included.

6 KAP average realized price: the weighted average price per pound for the total external sales of KAP HQ and THK. The pricing of intercompany transactions between KAP HQ and THK are not included.

7 Source: UxC, TradeTech. Amounts provided represent the average of the uranium spot prices quoted at month end, and not the average of each weekly quoted spot price. Contract price terms generally refer to a month-end price.

* Note that the conversion of kgU to pounds U3O8 is 2.5998.

On both a 100% and attributable basis, production volumes for the second quarter and first half of 2020 were modestly lower, as a result of the initial impact of decreased wellfield development activity and lower staff levels throughout the second quarter, amid the COVID-19 pandemic. There is typically a four to nine month lag between the wellfield development and production phases of the in-situ recovery mining process and as a result, the safety measures implemented during the first half of 2020 are expected to predominantly impact the second half of the year.

The year-over-year decrease in uranium sales at both the Group and KAP levels is due to seasonality and differences in the timing of deliveries for 2019 and 2020.

The rising uranium spot price had a positive impact on Kazatomprom’s average realized price, which increased in the second quarter and first half of the year. If spot prices remain higher than 2019, the trend of increasing realized price is expected to continue, with the Company’s delivery schedule weighted to the second half of 2020.

Kazatomprom’s 2020 Guidance

|

(exchange rate 450 KZT/1USD) |

2020 |

|

Production volume U3O8 (tU) (100% basis)1 |

19,000 – 19,5002 |

|

Production volume U3O8 (tU) (attributable basis)3 |

10,500 – 10 8002 |

|

Group sales volume (tU) (consolidated)4 |

15,500 – 16,500 |

|

Incl. KAP sales volume (incl. in Group) (tU)5 |

13,500 – 14,500 |

|

Revenue - consolidated (KZT billions)6 |

580 – 600 |

|

Revenue from Group U3O8 sales, (KZT billions)6 |

460 – 510 |

|

C1 cash cost (attributable basis) (USD/lb)* |

$10.00 - $11.00 |

|

All-in sustaining cash cost (attributable C1 + capital cost) (USD/lb)* |

$13.00 - $14.00 |

|

Total capital expenditures (KZT billions) (100% basis)7 |

65 - 75 |

1 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it disregards that some portion of production may be attributable to the Group’s JV partners or other third-party shareholders.

2 The duration and full impact of the COVID-19 pandemic is not yet known. Annual production volumes could therefore vary from our expectations, depending on the actual impact.

3 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, corresponding only to the size of such interest; it excludes the portion attributable to the JV partners or other third-party shareholders, except for JV “Inkai” LLP.The Company anticipates that the annual share of production in JV “Inkai” LLP in 2020 will be approximately 1,066 tU. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

4 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity)

5 KAP sales volume: includes only the total external sales of KAP HQ and THK. Intercompany transactions between KAP HQ and THK are not included.

6 Revenue expectations are based on uranium prices and KZT-to-USD exchange rate taken at a single point in time from third-party sources. The prices and KZT-to-USD exchange rate used do not reflect any internal estimate from Kazatomprom, and 2020 revenue could be materially impacted by how actual uranium prices and KZT-to-USD exchange rate vary from the third-party estimates.

7 Total capital expenditures (100% basis): includes only capital expenditures of the mining entities.

* Note that the conversion of kgU to pounds U3O8 is 2.5998.

All 2020 guidance remains unchanged at this time. Revenue, C1 cash cost (attributable basis) and All-in Sustaining cash cost (attributable C1 + capital cost) may vary from the ranges shown, to the extent that the KZT-to-USD exchange rate and uranium spot price differ from the assumptions shown in the footnotes.

Note that the Company only expects to update annual guidance in relation to operational factors and internal changes that are within its control. Key assumptions used for external metrics, such as exchange rates and uranium prices, are established in consultation with the major shareholder (Samruk-Kazyna) and from third party sources during the Company’s annual budget process; such assumptions will only be updated on an interim basis in exceptional circumstances.

The Company continues to target an ongoing inventory level of approximately six to seven months of annual attributable production. However, inventory levels are expected to fall below these levels in 2020 and 2021, with no opportunity to catch up production losses in these periods. As such, the Company will continue to monitor market conditions for opportunities to optimise its inventory levels and has purchased some volumes in the spot market at the end of the second quarter.

Conference Call Notification - 2020 Half-Year Operating and Financial Review (27 August 2020)

Kazatomprom has scheduled a conference call to discuss 2020 half-year operating and financial results, after they are released on Thursday, 27 August 2020. The call will begin at 17:00 (AST) / 12:00 (BST) / 07:00 (EST). Following management remarks, an interactive English Q&A session will be held with investors.

Interested parties are invited to join the live Q&A session using the following dial-in details:

- UK Participant Toll-Free Dial-In Number: +44 (0) 80 0028 8438

- UK Participant Local Dial-In Number: + 44 (0) 20 3107 0289

- US Participant International US-Toll Dial-In Number: +1 (918) 922-6506

To participate in live Q&A, provide the conference ID number 2950189 when prompted.

A live webcast of the conference call will be available from a link at www.kazatomprom.kz home page on the day of the call. Participants can also ask questions using the webcast question feature.

A recording of the webcast will also be available at www.kazatomprom.kz shortly after the event.

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Cory Kos, Director of Investor and Public Relations

Tel: +7 (8) 7172 45 81 80

Email: ir@kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Torgyn Mukayeva, Deputy Director of Investor and Public Relations

Tel: +7 (8) 7172 45 80 63

Email: pr@kazatomprom.kz

About Kazatomprom

Kazatomprom is the world's largest producer of uranium, with the company’s attributable production representing approximately 24% of global primary uranium production in 2019. The Group benefits from the largest reserve base in the industry and operates, through its subsidiaries, JVs and Associates, 24 deposits grouped into 13 mining assets. All of the Company’s mining operations are located in Kazakhstan and mined using ISR technology with a focus on maintaining industry-leading health, safety and environment standards.

Kazatomprom securities are listed on the London Stock Exchange and Astana International Exchange. As the national atomic company in the Republic of Kazakhstan, the Group's primary customers are operators of nuclear generation capacity, and the principal export markets for the Group's products are China, South and Eastern Asia, Europe and North America. The Group sells uranium and uranium products under long-term contracts, short-term contracts, as well as in the spot market, directly from its headquarters in Nur-Sultan, Kazakhstan, and through its Switzerland-based trading subsidiary, Trade House KazakAtom AG (THK).For more information, please see our newly updated website at http://www.kazatomprom.kz

Forward-looking statements

All statements other than statements of historical fact included in this communication or document are forward-looking statements. Forward-looking statements give the Company’s current expectations and projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plan,” “project,” “will,” “can have,” “likely,” “should,” “would,” “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future. THE INFORMATION WITH RESPECT TO ANY PROJECTIONS PRESENTED HEREIN IS BASED ON A NUMBER OF ASSUMPTIONS ABOUT FUTURE EVENTS AND IS SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTY AND OTHER CONTINGENCIES, NONE OF WHICH CAN BE PREDICTED WITH ANY CERTAINTY AND SOME OF WHICH ARE BEYOND THE CONTROL OF THE COMPANY. THERE CAN BE NO ASSURANCES THAT THE PROJECTIONS WILL BE REALISED, AND ACTUAL RESULTS MAY BE HIGHER OR LOWER THAN THOSE INDICATED. NONE OF THE COMPANY NOR ITS SHAREHOLDERS, DIRECTORS, OFFICERS, EMPLOYEES, ADVISORS OR AFFILIATES, OR ANY REPRESENTATIVES OR AFFILIATES OF THE FOREGOING, ASSUMES RESPONSIBILITY FOR THE ACCURACY OF THE PROJECTIONS PRESENTED HEREIN. The information contained in this communication or document, including but not limited to forward-looking statements, applies only as of the date hereof and is not intended to give any assurances as to future results. The Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to such information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date hereof.