JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the third quarter and nine months ended 30 September 2022.

This update provides a summary of recent developments in the uranium and nuclear industries, as well as provisional information related to the Company’s key third-quarter and nine-month operating and trading results, and updated 2022 guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

In September, the annual World Nuclear Association Symposium, held in-person in London, UK for the first time in three years, featured industry experts and panels focused on the significance of preserving the current global nuclear fleet, while working to enhance nuclear power’s role in achieving the United Nations' climate goals. Social perception of nuclear power and its benefits, and general sentiment within the uranium market have grown increasingly positive, with a significant portion of the Symposium spent discussing opportunities for the sector to play a crucial role in the effort to reduce global carbon emissions. The Symposium sessions also covered the evolving political dynamics in the context of the Russia-Ukraine conflict, which has driven many nations to revise energy security policies and consider or reconsider the use of nuclear energy as a safe, reliable, scalable, and low-carbon energy source.

In September, Japan announced plans to restart seven additional nuclear reactors as soon as possible to ensure a steady supply of power across the country. To prepare for possible electricity supply shortfalls, the ministry indicated that it would like to see a total of 17 nuclear reactors operating and online, including the ten reactors that have already received operating approval. In a related development, Japan's Nuclear Regulation Authority (NRA) stated that it also plans to extend the current maximum 60-year operating life limitation for the nation’s reactors. According to current Japanese legislation, reactors can operate for a maximum of 40 years with only one potential 20-year extension following a thorough screening process.

China's State Council officially approved the construction of unit 1 and unit 2 (Phase I) at the Lianjiang nuclear facility in Guangdong Province, and unit 3 and unit 4 (Phase II) at the Zhangzhou plant in Fujian Province, with the new nuclear projects included in China's national energy plans. Lianjiang is a new plant operated by China's State Power Investment Corporation (SPIC) and Phase I will utilize China’s domestically designed 1,161 MWe CAP-1000 PWR, an adapted version of the Westinghouse AP-1000. The Phase II project at Zhangzhou will be managed by China National Nuclear Power (CNNP), a division of China National Nuclear Corporation. The new Zhangzhou units are expected to be the HPR-1000 (Hualong One) reactor design.

In the US, the 2022 Inflation Reduction Act (IRA) authorized by the US President in August, includes broad technology-neutral tax credits for carbon-free energy sources, which is expected to benefit future reactors as well as providing tax credits for nuclear power facilities that are currently in operation. The law also allocates $700 million to support the creation of domestic high-assay low-enriched uranium (HALEU) capacity and nearly $400 billion for clean energy and climate change-related initiatives in the United States. The IRA also offers support for the development of small modular reactors and advanced reactors, with incentives for building such nuclear facilities to replace retired coal-fired and other fossil fuel plants or mining operations.

During the third quarter, a number of demand-side highlights emerged:

- In the UK, Hinkley Point B unit 1 and unit 2 were permanently shut down on 06 July and 01 August respectively, after more than 46 years of safe operation in Somerset. Hinkley Point B, which began operation in 1976 and comprises two 660 MWe advanced gas-cooled reactors (AGRs), generated around 311TWh of electricity over its lifetime.

- According to a subsidiary of SPIC, construction of Haiyang unit 3 in Shandong Province, China, began on 07 July. The Haiyang facility comprises two existing operating Westinghouse AP-1000 PWRs (unit 1 and unit 2) while units 3 and unit 4 will be domestically designed CAP-1000 PWRs.

- China General Nuclear (CGN) announced that the Lufeng facility in Guangdong Province, China, saw the official start of construction in September, with the first nuclear safety-related concrete poured for unit 5. The new Lufeng unit 5 reactor uses China’s domestic HPR-1000 (Hualong One) PWR design.

- In July, Rosatom announced it had begun construction of a new VVER-1200 PWR at the Akkuyu nuclear plant in Turkey, with the pouring of first nuclear safety-related concrete at unit 4. The Akkuyu facility now comprises four units simultaneously under construction by Rosatom and it is the first nuclear plant under construction in the Republic of Turkey.

- According to Rosatom, first concrete for nuclear safety-related purposes was poured in July for El Dabaa unit 1, signaling the start of construction for the first commercial nuclear plant in Egypt. When completed, the plant will host four 1,200 MWe VVER-1200 PWRs.

- With rising summer temperatures and anticipated energy shortages, lawmakers in California approved legislation giving Pacific Gas & Electric Company, the operator of the state's last operating nuclear power plant, Diablo Canyon, a $1.4 billion loan to extend the plant's life for five more years (until 2030).

- In Mexico, the Laguna Verde nuclear power plant in Veracruz received a 30-year operating extension, according to a report from the Comisión Federal de Electricidad. The license extension, granted in August, is valid until 10 April, 2055.

Subsequent to the end of the third quarter, Emirates Nuclear Energy Corporation reported in early October that unit 3 of the Barakah facility in Abu Dhabi, United Arab Emirates, had been connected to the grid. Barakah unit 3 is one of four 1,400 MWe APR-1400 PWRs reactors constructed at the facility by South Korea’s KEPCO.

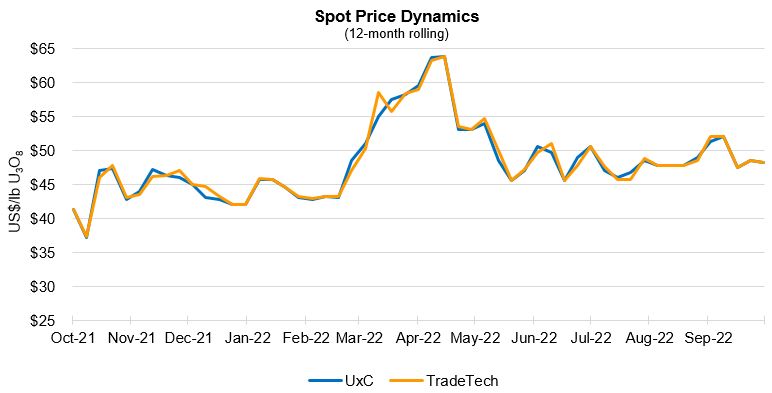

Market Pricing and Activity

Although uranium spot market activity is usually slower throughout the summer months, contracting interest during the summer of 2022 was particularly quiet due to utility customers shifting their attention to potential bottlenecks in the conversion and enrichment segments, as they seek to reduce reliance on Russian processing services. Uranium spot activity was very limited throughout July and August, with the spot price ranging between US$45.00/lb U3O8 and US$50.00/lb U3O8. Activity in the spot market picked up in September pushing the price to US$52.00/lb U3O8. However, with equity markets under pressure and a sharp decline in purchasing activity by financials entities, the price fell back to about US$48.00/lb U3O8 by the end of the quarter.

According to third-party market data, spot volumes transacted over the first nine months of 2022 were about 40% lower than the same period last year. A total of approximately 41 million pounds U3O8 (15,800 tU) was transacted at an average weekly spot price of US$49.67/lb U3O8, compared to about 71 million pounds U3O8 (27,300 tU) at an average weekly spot price of US$31.96/lb U3O8 during the first nine months of 2021.

In the term market, third-party data indicated that contracted volumes totalled about 80 million pounds U3O8 (30,600 tU) through the first nine months of 2022, compared to about 53 million pounds U3O8 (20,200 tU) in the same period of 2021. The 50% increase in term contracting activity to date in 2022 led to a significant US$8.50/lb U3O8 increase of the long-term price indicator at the end of the third quarter, resulting in an average term price of US$51.50/lb U3O8 (reported on a monthly basis by third-party sources).

Company Developments

Transportation risk

Kazatomprom continues to monitor the growing list of sanctions on Russia and the potential impact they could have on the transportation of products through Russian territory. To date, there are no restrictions on the Company's activities related to the supply of its products to customers worldwide. Kazatomprom shipped its third quarter volumes via St. Petersburg without any disruptions or logistical/insurance-related issues. However, the Trans-Caspian International Transport Route (TITR), which the Company has successfully used as an alternative route since 2018, helps to mitigate the risk of the primary route being unavailable, for any reason.

In order to transport Class 7 nuclear material on the TITR, permits must be issued by the relevant authorities in the jurisdictions through which the material passes. Kazatomprom has an approved quota allowing the Company to ship a total of up to 3,500 tU from its Kazakh mines via the TITR. The Company is working to increase the quota limit and is assisting JV partners if they would prefer not to receive their share of material via the established route that passes through the Port of St. Petersburg.

The TITR requires the use of chartered sea vessels on the Black Sea rather than commercial shipping companies. In order to maximize the cost efficiency of using a chartered vessel, material must be consolidated at the Georgian Port of Poti.

Kazatomprom currently has a shipment to western markets in-progress on the TITR; the KAP-owned portion of the shipment has reached the Port of Poti without issue and it is now waiting for additional material to arrive, prior to being loaded onto a vessel for furtherance to its final destination. Kazatomprom’s past and current shipments of KAP-owned material are permitted based on commitments directly between KAP and the end-user taking title of the material at the destination. However, when shipping Kazakh-origin uranium from JV operations to JV partners using the TITR, transit country authorities ask for certain shipment details and associated documents, provided by the Kazakh JV and potentially, from its non-KAP JV partner. As it is the first time the TITR-related jurisdictions are reviewing such arrangements, there is an elevated risk of transportation delays. The shipment that is currently en route to join Kazatomprom’s material waiting at the Port of Poti is sourced from JV Inkai and it has been delayed. There is a risk that the Company’s 2022 guidance for consolidated sales and consolidated revenue could be impacted if that portion of the shipment and/or if future shipments on the TITR in 2022, are delayed.

Whether shipped by Kazatomprom or its partners sharing Kazakh assets, the product remains of Kazakh origin through to its arrival at a western conversion facility.

Sulfuric acid plant feasibility

Kazatomprom presented its potential investment plan for a new sulfuric acid plant to the Prime Minister of the Republic of Kazakhstan, Alikhan Smailov, during his trip to the Turkestan region in October 2022. Detailed feasibility work is underway to confirm acid requirements and estimate the anticipated construction schedule and capital costs.

The implementation of the project is expected to take place between 2022 to 2026 (including the feasibility work currently underway). The facility is expected to be built in the Sozak district of the Turkestan region in Kazakhstan, which is in close proximity to some of Kazatomprom’s mines that do not have railway access and it would therefore significantly shorten acid delivery routes.

2024 Production Plans

As previously disclosed in August, Kazatomprom’s Board of Directors approved a strategy to revise the Company’s 2024 production volume down by approximately 10% compared to the total Subsoil Use Contract level of 28,691 tU, disclosed in its most recent 2021 Competent Person’s Report (“2021 CPR”).

The decision to shift production from minus 20% in 2023 to approximately minus 10% in 2024 is based primarily on Kazatomprom’s continued success in signing mid- and long-term contracts with new and existing customers. The current contract book provided sufficient confidence that the additional volumes in 2024 will have a secure place in the market and be needed to fulfill future contractual obligations.

The full implementation of this decision could remove approximately 3,500 tU from anticipated global primary supply in 2024. Kazatomprom’s 2024 production is therefore expected to be between 25,000 tU and 25,500 tU (100% basis), compared to the total Subsoil Use Contracts level for 2024 of 28,691 tU, disclosed in the 2021 CPR. Although the year-over-year production increase from 2023 to 2024 is modest, the Company may face significant challenges to any increase above current production levels, based on the current state of global supply chains and the availability of key operating materials.

Chief Executive Officer (“CEO”) and Management Board

As previously disclosed, the Company’s Board of Directors approved the appointment of Mr. Yerzhan Mukanov, acting CEO since July and Chief Operations Officer (“COO”) since March 2022, as Kazatomprom’s CEO and Chair of the Company’s Management Board. With the promotion of Mr. Mukanov to CEO, the Company, with the support of the Board of Directors, has initiated a recruitment process to assess appropriate candidates for the vacant COO position.

In connection with the appointment of Mr. Mukanov as Chairman of Kazatomprom’s Management Board, the issue of electing of Mr. Mukanov as a member of Kazatomprom Board of Directors was proposed for approval by Company Shareholders at a virtual EGM on 01 November 2022. The notice of the upcoming EGM, as well as the ballot for absentee voting are available on the Company's website.

Full biographies of Kazatomprom’s Management Board members are available on the Company’s website, https://www.kazatomprom.kz

Kazatomprom’s 2022 Third-Quarter and Nine-Month Operational Results1

|

|

Three months ended September 30 |

|

Nine months ended September 30 |

|

||

|

(tU as U3O8 unless noted) |

2022 |

2021 |

Change |

2022 |

2021 |

Change |

|

Production volume (100% basis)2 |

5,377 |

5,508 |

-2% |

15,446 |

15,960 |

-3% |

|

Production volume (attributable basis)3 |

2,895 |

2,928 |

-1% |

8,309 |

8,792 |

-5% |

|

Group sales volume4 |

4,316 |

2,215 |

95% |

13,332 |

8,409 |

59% |

|

KAP sales volume (incl. in Group)5 |

4,200 |

1,619 |

159% |

12,232 |

6,798 |

80% |

|

Group average realized price (USD/lb U3O8)6* |

46.10 |

32.10 |

44% |

42.60 |

30.27 |

41% |

|

KAP average realized price (USD/lb U3O8)7* |

46.08 |

31.68 |

45% |

41.98 |

29.99 |

40% |

|

Average month-end spot price (USD/lb U3O8)8* |

49.13 |

35.98 |

37% |

49.77 |

31.96 |

56% |

1 All values are preliminary.

2 U3O8 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it therefore disregards the fact that some portion of that production may be attributable to the Group’s joint venture partners or other third- party shareholders. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 U3O8 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, which corresponds only to the size of such interest; it therefore excludes the remaining portion attributable to the JV partners or other third-party shareholders, except for production from JV “Inkai” LLP, where the annual share of production is determined as per the Implementation Agreement disclosed in the IPO Prospectus. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

4 Group U3O8 sales volume: includes the sales of U3O8 by Kazatomprom and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity). Group U3O8 sales volumes do not include other forms of uranium products (including, but not limited to, the sales of fuel pellets).

5 KAP U3O8 sales volume (incl. in Group): includes only the total external sales of U3O8 of KAP and Trade House KazakAtom AG (THK). Intercompany transactions between KAP and THK are not included.

6 Group average realized price (USD/lb U3O8): average includes Kazatomprom’s sales and those of its consolidated subsidiaries, as defined in footnote 4 above.

7 KAP average realized price (USD/lb U3O8): the weighted average price per pound for the total external sales of KAP and THK. The pricing of intercompany transactions between KAP and THK are not included.

8 Source: UxC LLC, TradeTech. Values provided are the average of the month-end uranium spot prices quoted by UxC and TradeTech, and not the average of each weekly quoted spot price throughout the month. Contract price terms generally reference month-end prices.

* Note the conversion of kgU to pounds U3O8 is 2.5998.

Production on both a 100% and attributable basis were slightly lower in the third quarter and for the first nine months of 2022 compared to the same periods in 2021, primarily due to the impact of the COVID-19 pandemic on wellfield development in 2021. There is typically an eight- to ten-month lag between wellfield development and the resulting uranium extraction by in-situ recovery, therefore the 2021 delays and/or limited access to certain key materials and equipment that affected wellfield commissioning schedules resulted in lower production several months later in 2022. Additionally, attributable production was impacted by the sale of a 49% share of “Ortalyk” LLP to CGN Mining UK Limited in July 2021.

In the third quarter and first nine months of 2022, both Group and KAP sales volumes were significantly higher compared to the same periods in 2021, primarily due to the timing of customer-scheduled deliveries. Sales volumes can vary substantially each quarter, and quarterly sales volumes vary year to year due to variable timing of customer delivery requests during the year, and physical delivery activity.

Average realized prices for both the third quarter and first nine months of 2022 were higher compared to the same periods in 2021 due to a higher uranium spot price. The Company’s current overall contract portfolio pricing correlates closely to uranium spot prices. However, for short-term deliveries to end-user utilities, the spot price can vary between the time contract pricing is established according to Kazakh transfer pricing regulations, and the spot price in the general market when the actual delivery takes place. The impact of market volatility during the time lag between price-setting and delivery becomes more pronounced as volatility increases, in both rising and falling price conditions. In addition, some long-term contracts incorporate a proportion of fixed pricing negotiated prior to the sharp increase in spot price over the last 12 months. As a result, increases in both the Group and KAP’s average realized prices in the third quarter and first nine months of 2022, compared to the same periods in 2021, were lower than the increases in the spot market price for uranium over the same intervals.

Kazatomprom’s 2022 Updated Guidance

|

(exchange rate 460 KZT/1USD) |

2022 |

|

Production volume U3O8 (tU) (100% basis)1 |

21,000 – 22,0002 |

|

Production volume U3O8 (tU) (attributable basis)3 |

10,900 – 11,5002 |

|

Group U3O8 sales volume (tU) (consolidated)4 |

16,300 – 16,8005 |

|

Incl. KAP U3O8 sales volume (incl. in Group) (tU) |

13,400 – 13,9005 |

|

Revenue - consolidated (KZT billions)6 |

930 – 9505 |

|

Revenue from Group U3O8 sales (KZT billions)6 |

790 – 810 |

|

C1 cash cost (attributable basis) (USD/lb)* |

$9.50 – $11.00 |

|

All-in sustaining cash cost (attributable C1 + capital cost) (USD/lb)* |

$16.00 – $17.50 |

|

Total capital expenditures of mining entities (KZT billions) (100% basis)7 |

150-160 (previously 160-170) |

1 Production volume U3O8 (tU) (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it disregards that some portion of production may be attributable to the Group’s JV partners or other third-party shareholders.

2 The duration and full impact of the COVID-19 pandemic and the Russian-Ukrainian conflict are not yet known. Annual production volumes could therefore vary from expectations.

3 Production volume U3O8 (tU) (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, corresponding only to the size of such interest; it excludes the portion attributable to the JV partners or other third-party shareholders, except for JV “Inkai” LLP, where the annual share of production is determined as per Implementation Agreement disclosed in the IPO Prospectus.

4 Group sales volume: includes the sales of U3O8 by Kazatomprom and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity). Group U3O8 sales volumes do not include other forms of uranium products (including, but not limited to, the sales of fuel pellets).

5 KAP sales volume: includes only the total external sales of U3O8 of KAP and THK. Intercompany transactions between KAP and THK are not included.

6 Revenue expectations are based on a uranium prices taken from third-party sources at a single point in time and on an exchange rate assumption of KZT460:USD1. There continues to be significant volatility in both uranium price and the tenge exchange rate. Therefore, 2022 revenue could be materially impacted if actual uranium prices and exchange rates vary from the third-party and internal estimates, respectively.

7 Total capital expenditures (100% basis): includes only capital expenditures of the mining entities.

* Note that the conversion of kgU to pounds U3O8 is 2.5998.

COVID-19 disrupted the overall production supply chain in 2021, resulting in a shortage of certain production materials, such as reagents and piping, which led to a shift in the commissioning schedule for new wellfields. Because of the shift, uranium production volumes through the first nine months of 2022 fell short of internal expectations. In addition to the delays in the commissioning schedule for new wellfields, shortages of certain materials, including sulfuric acid, also have a negative impact on development and production activities. Despite these challenges, the Group is maintaining its 2022 production plan and making every effort to achieve it, though final year-end volumes could fall short if wellfield development and supply chain issues continue throughout the fourth quarter of the year.

Aside from guidance for Total capital expenditures of mining entities, all other 2022 guidance metrics remain unchanged from previous expectations. After nine months, capital spending continues to trend below budgeted levels due to the postponement of development drilling, piping and acidification as a result of limited access to certain key operating materials and equipment, including sulfuric acid and pipes. The related activity and capital expenditures will be shifted from 2022 to 2023, which, due to the nature of the in-situ recovery mining method, does not directly impact 2022 production, but is expected to impact 2023 and 2024 mine development and production schedules.

Revenue, C1 cash cost (attributable basis) and All-in Sustaining cash cost (attributable C1 + capital cost) may vary from the ranges shown, to the extent that the KZT-to-USD exchange rate and uranium spot price differ significantly from the Company’s assumptions.

As was explained in the Company developments section above, if shipments from JV Inkai are delayed beyond year-end, Consolidated Group U3O8 sales volume could be negatively impacted (reduced by a quantity up to the partner’s attributable share that is delayed). However, the Company expects Revenue - consolidated and Revenue from Group U3O8 sales to remain within the guided ranges, due to the average realized price being higher than budgeted, which is expected to partially offset the potential revenue impact.

The Company only intends to update annual guidance in relation to operational factors and internal changes that are within its control. Key assumptions used for external metrics, such as exchange rates and uranium prices, are established using third-party sources during the Company’s annual budget process in the previous year and such assumptions will only be updated on an interim basis in exceptional circumstances.

The Company continues to target an inventory level of approximately six to seven months of annual attributable production. However, inventory could fall below these levels due to Pandemic-related production losses. As such, during the third quarter, several transactions to purchase material in the spot market were carried out and the Company will continue to monitor market conditions for opportunities to optimize its inventory levels.

Kazatomprom Analyst Day (26 October 2022)

Today, 26 October 2022, Kazatomprom is holding its 2022 Analyst Day at the Company headquarters in Astana, Kazakhstan. The event will begin at 5 pm local time / 12 pm BST / 7 am EDT.

The live event and webcast will be in English only; a translated Russian transcript will be made available the following week on Kazatomprom’s official webpage, www.kazatomprom.kz.

To view Kazatomprom’s Analyst Day live webcast, please see the link below:

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Cory Kos, International Adviser, Investor Relations

Botagoz Muldagaliyeva, Director of Investor Relations

Tel: +7 (8) 7172 45 81 80/69

Email: ir@kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Sabina Kumurbekova, Director, GR & PR Department

Gazhaiyp Kumisbek, Chief Expert, GR & PR Department

Tel.: +7 7172 45 80 22

Email: pr@kazatomprom.kz

A copy of this announcement is available at www.kazatomprom.kz.

About Kazatomprom

Kazatomprom is the largest uranium producer in the world with natural uranium production in proportion to the Company's participatory interest in the amount of about 24% of the total global primary uranium production in 2021. The group has the largest uranium reserve base in the industry. Kazatomprom, together with subsidiaries, affiliates and joint organizations, is developing 26 deposits combined into 14 uranium-mining enterprises. All uranium mining enterprises are located on the territory of the Republic of Kazakhstan and when mine uranium use in-situ recovery technology, paying particular attention to best HSE practices and means (ISO 45001 and ISO 14001 certified).

Kazatomprom's securities are listed on the London Stock Exchange, the Astana International Exchange and the Kazakhstan Stock Exchange. Kazatomprom is the National Atomic Company of the Republic of Kazakhstan, and the main customers of the group are operators of nuclear generating capacities, and the main export markets for products are China, South and East Asia, North America and Europe. The Group sells uranium and uranium products under long-term and short-term contracts, as well as on the spot market directly from its corporate centre in Astana, Kazakhstan, as well as through a trading subsidiary in Switzerland, Trading House KazakAtom (THK).

For more information, please, visit our website http://www.kazatomprom.kz

Statements for the Future

All statements, other than statements of historical fact, included in this message or document are statements regarding the future. Statements regarding the future reflect the Company's current expectations and estimates regarding its financial condition, results of operations, plans, goals, future results and activities. Such statements may include, but are not limited to, statements before which, after which or where words such as “goal”, “believe”, “expect”, “intend”, “possibly”, “anticipate”, “evaluate”, “plan”, “project”, “will”, “may”, “probably”, “should”, “may” and other words and terms of a similar meaning or their negative forms are used.

Such statements regarding the future include known and unknown risks, uncertainties and other important factors beyond the control of the Company, which may lead to the fact that the actual results, indicators or achievements of the Company will significantly differ from the expected results, indicators or achievements expressed or implied by such statements regarding the future. Such statements regarding the future are based on numerous assumptions regarding the current and future business strategy of the Company and the conditions in which it will operate in the future.

INFORMATION ON THE ESTIMATES CONTAINED IN THIS DOCUMENT ARE BASED ON SEVERAL ASSUMPTIONS ABOUT FUTURE EVENTS AND ARE SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTIES AND OTHER CONVENTIONALITIES, NONE OF WHICH CAN NOT BE PREDICTED WITH CERTAINTY AND SOME OF WHICH ARE OUTSIDE OF THE COMPANY'S CONTROL. THERE CAN NOT BE ANY WARRANTY THAT THE ESTIMATES WILL BE REALIZED AND THE ACTUAL RESULTS MAY BE ABOVE OR BELOW THAN SPECIFIED. NONE OF THE COMPANY - NO SHAREHOLDERS, NO DIRECTORS, NO OFFICERS, NO EMPLOYEES, NO CONSULTANTS, NO AFFILIATES NOR ANY REPRESENTATIVES OR AFFILIATES LISTED ABOVE BEAR RESPONSIBILITY FOR THE ACCURACY OF THE ESTIMATES PRESENTED IN THIS DOCUMENT.

The information contained in this message or document, including, but not limited to, statements regarding the future, is applicable only as of the date of this document and is not intended to provide any guarantees regarding future results The Company expressly disclaims any obligation to disseminate updates or changes to such information, including financial data or forward-looking statements, and will not publicly release any changes that it may make to information arising from changes in the Company's expectations, changes in events, conditions or circumstances on which such statements regarding the future are based, or in other events or circumstances arising after the date of this document.