JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the third quarter and nine months ended 30 September 2023.

This update provides a summary of recent developments in the uranium industry, as well as provisional information related to the Company’s key third-quarter and nine-month operating and trading results, and updated 2023 guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

Earlier in September nuclear industry leaders, experts and key market players gathered in London for the annual World Nuclear Symposium to discuss major issues, current problems and prospectives of nuclear fuel market. The updated hallmark market reports were presented, and several initiatives and campaigns were introduced to the public. In order to achieve "unprecedented collaboration between governments, industry leaders, and civil society" in advance of COP28, the World Nuclear Association and the Emirates Nuclear Energy Corporation (ENEC) have launched the Net Zero Nuclear initiative with the help of Atoms4NetZero of the International Atomic Energy Agency and the UK government. The campaign's goal is to ensure nuclear energy's potential "is fully realized in facilitating the decarbonization of global energy systems by promoting the value of nuclear energy and removing barriers to its growth," particularly ahead of UN Climate Change Conference, which will take place in the United Arab Emirates later this year.

Along with the Net Zero Nuclear initiative several policy developments have been announced in the third quarter:

- On 18 July 2023, the UK Department of Energy Security has announced the launch of the Great British Nuclear programme, aimed at stimulating the rapid expansion of new nuclear power plants in the country, under which funding could reach up to £20 billion (~US$25.8 billion).

- On 27 July 2023, the U.S. Senate voted to approve the National Defense Authorization Act (NDAA), which allows funding and sets policy objectives for the Department of Defense (DoD). A bipartisan addition to the NDAA was also voted in favor by senators and calls for the U.S. DOE to prioritise initiatives to boost domestic production of Low-Enriched Uranium (LEU) for operating reactors and quicken steps to secure the availability of High-Assay Low-Enriched Uranium (HALEU).

- The Swedish government plans to lift restrictions on the number of commercial nuclear reactors, and simplify the procedure for obtaining permits for the construction of new reactors. According to the government, in 2030-2040 Sweden will require commissioning new nuclear capacity, equivalent of 10 full-scale reactors, to satisfy the growing national electricity demand.

- Italian government has restated its ambition of reviving the Italian nuclear energy industry, with several ministers announcing plans to restart nuclear generation within the next 10 years. Reviving nuclear power in Italy is seen as an aid to the green transition of the country. Earlier this year, the government supported a French-sponsored alliance of pro-nuclear EU countries.

In addition to policy updates, numerous announcements regarding demand-side were made during the reported period:

- Tricastin Unit 1, EDF-operated nuclear reactor in the southern region of France, becomes the first French power reactor licensed to operate beyond 40 years.

- Westinghouse and Bechtel have signed a formal partnership agreement for the design and construction of Poland's first nuclear power plant at the Lubiatowo-Kopalino site. Poland’s first AP1000 nuclear reactor is anticipated to achieve commercial operation in 2033.

- Pakistan has begun construction of the fifth unit of the Chashma nuclear power plant in Punjab, costing about $3.5 billion, with a capacity of 1,200 MWe, which will be equipped with a Chinese Hualong One reactor. Construction is expected to be completed by 2030.

- Kansai Electric Power Co. (Kansai) restarted the first power unit of 780 MWe at the Takahama nuclear power plant in Fukui Prefecture, Japan, which was decommissioned more than 12 years ago. Consequently, in September, Kansai restarted a 47-year-old reactor at its western nuclear power plant of Takahama, adding nearly 1 GWe of power to the grid. Following special government approval to extend its life beyond the standard limit of 40 years, the Takahama No.2 reactor becomes Japan's third of the kind to come back online after Kansai Electric's Mihama No.3 and Takahama No.1.

- China has approved the construction of six new reactors at three operating nuclear power plants – Units 5 and 6 of Ningde Nuclear Power Plant, Units 1 and 2 of Shidaowan Nuclear Power Plant, and Units 1 and 2 of Xudapu Nuclear Power Plant. These are China's first permits for the construction of reactors in 2023 (permits for 10 reactors in 2022).

- Georgia Power has started loading fuel into Unit 4 at Vogtle Nuclear Power Plant, marking the full start-up of the second new reactor in the U.S. state of Georgia. However, due to malfunction of the coolant pump, commercial operation of Vogtle 4 is postponed to the next year.

- Slovakia's Mochovce Nuclear Power Plant Unit 3 achieved 100% power output in recent tests. Unit 3 is expected to come into commercial operation in the coming months. Block 4 should be launched approximately one to two years after Block 3.

- Argentina's Atucha 2 reactor was restarted after 10 months of shutdown due to repair work.

- Rosatom has begun the main stage of construction of two new VVER-1200 units at the Paks II NPP in Hungary. The total reactor power will amount to 2.4 GWe.

- CGN announced the start of construction of the sixth HPR1000 unit at the Lufeng Nuclear Power Plant.

- The Egyptian government has approved the construction of the fourth unit at the Dabaa nuclear power plant.

- Westinghouse Electric has announced the delivery of the first batch of VVER-440 fuel assemblies to the Ukrainian state energy company Energoatom.

- Bangladesh takes delivery of the first batch of fabricated fuel assemblies for the Rosatom-built Unit 1 of the Rooppur nuclear power plant. Bangladesh will become the world’s 33rd nuclear country after the Rooppur begins its commercial startup.

- On September 6, 2023, Centrus Energy Corp. declared that it anticipates starting HALEU production at the American Centrifuge Plant in Piketon, Ohio, in October 2023 – roughly two months earlier than planned. The 16-centrifuge cascade, which is anticipated to start enrichment operations in October, will only be able to process roughly 900 kg of HALEU annually. After obtaining the required funds, a full-scale HALEU cascade with 120 centrifuges and a combined capability to generate about 6,000 kg of HALEU annually (6 MTU/year) may be put online in about 42 months.

On the supply side developments, due to the military coup in Niger, Canadian uranium producer Global Atomic Corporation is considering delaying the commissioning of the processing plant at the Dasa project by 6–12 months.

Also, in related news, in September Orano announced that it was forced to reschedule maintenance work at its SOMAIR uranium plant in Niger due to depletion of chemical supplies amid continued inaccessibility of the main material supply corridor to Niger. It was reported earlier that Orano was halting the processing of uranium ore at its facility because international sanctions against the military junta are hampering logistics.

In its Production and Market Update for the third quarter of 2023, Cameco announced a decrease in its expected production volume for 2023 due to technical issues: instead of the planned 18 million pounds at Cigar Lake mine, the company expects to produce 16.3 million pounds of U3O8, while production on recently restarted McArthur river is expected to be down 1 million pounds.

Market Pricing and Activity

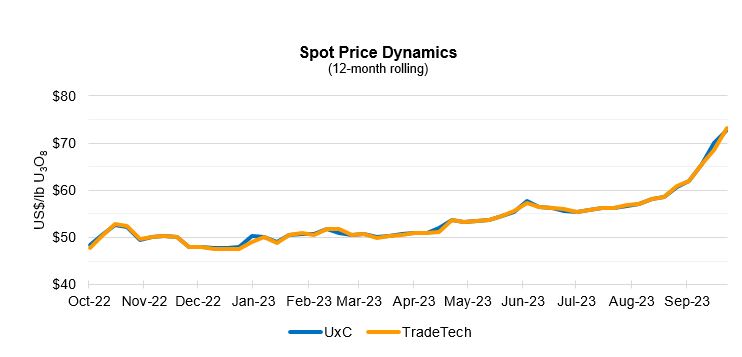

The spot uranium market was largely quiet in July and most of August, however, the final week of August saw a considerable increase in transactional activity. In September, the market showed a steady price rise, which was already experiencing upward price pressure as a result of the situation in Niger and unmet targets by both established and new producers. Consequently, the prices surged beyond the US$70 mark to hit US$73.50/lb U3O8, which was the highest level since March 2008. According to third-party market data, spot volumes transacted over the first nine months of 2023 were about 20% lower compared to the same period last year. During the nine months of 2023, a total of approximately 32 million pounds U3O8 (12,400 tU) were transacted at an average weekly spot price of US$54.67/lb U3O8, compared to about 41 million pounds U3O8 (15,800 tU) at an average weekly spot price of US$49.67/lb U3O8 over the first nine months of 2022.

In the term market, third-party data indicated that contracted volumes totaled to about 145 million pounds U3O8 (55,700 tU) throughout the first nine months of 2023, compared to about 85 million pounds U3O8 (32,700 tU) in the same period of 2022. The 70% increase in term contracting activity to date in 2023 led to a significant US$10.50/lb U3O8 increase of the long-term price indicator at the end of the third quarter, resulting in an average term price of US$61.50/lb U3O8 (reported on a monthly basis by third-party sources).

Company Developments

Transportation risk mitigation

Kazatomprom continues to monitor the list of sanctions on Russia and the potential impact they could have on the transportation of products through Russian territory. To date, there are no restrictions on the Company's activities related to the supply of its products to customers worldwide. Kazatomprom shipped its third quarter volumes without any disruptions or logistical/insurance-related issues. The Trans-Caspian International Transport Route (TITR), which the Company has successfully used as an alternative route since 2018, helps to mitigate the risk of the primary route being unavailable, for any reason.

As previously disclosed, within the framework of WNA’s Transport Working Group Kazatomprom provided an update on the status of TITR deliveries. The Company highlighted that as of the first half of 2023, 58% of all shipments of uranium from Kazakhstan to Western countries were shipped through TITR. It is expected that for the full year of 2023 the total share of TITR shipments in Kazatomprom’s deliveries of uranium to Western countries will amount to up to 71%.

Whether shipped by Kazatomprom or its JV partners, Kazakh-origin uranium retains its origin until its arrival at a conversion facility.

Management Board Composition Update

On 28 September 2023, Kazatomprom's Board of Directors has appointed Mr. Meirzhan Yussupov as Kazatomprom’s new Chief Executive Officer (“CEO”) and Chairman of the Management Board effective 02 October 2023. The Company’s Board has also approved the appointment of Mr. Sultan Temirbayev, Kazatomprom’s CFO, to the Management Board.

Kazatomprom's Management Board currently consists of:

- Meirzhan Yussupov, Chief Executive Officer;

- Kuanysh Omarbekov, Chief Operating Officer;

- Dastan Kosherbayev, Chief Commercial Officer;

- Sultan Temirbayev, Chief Financial Officer;

- Yermek Kuantyrov, Chief Legal Support and Corporate Governance Officer;

- Alibek Aldongarov, Chief HR and HSE Officer;

- Mukhit Magazhanov, Chief Procurement and General Affairs Officer.

Board of Directors Composition Update

On 1 November 2023, the Company’s Shareholders at Extraordinary General Meeting (EGM) appointed Meirzhan Yussupov, the Company’s CEO, and Aidar Ryskulov, representing the interests of majority shareholder Samruk-Kazyna JSC, as members of Kazatomprom’s Board of Directors. The terms being set until the expiration of the current term of office of the Board of Directors – 20 June 2026. The newly elected member of the Board of Directors representing the interests of majority shareholder of Samruk-Kazyna JSC, Mr. Ryskulov, will replace Yernar Zhanadil in this post.

In addition, shareholders at the EGM have appointed Mr. Aidar Ryskulov as a member of the Strategic Planning and Investment Committee due to the resignation of Mr. Zhanadil.

Kazatomprom's Board of Directors currently consists of:

- Arman Argingazin – Independent Non-Executive director, Chairman of the Board of Directors;

- Armanbay Zhubaev – Independent Non-Executive director;

- Nodir Sidikov – Independent Non-Executive director;

- Yernat Berdigulov – Representative of Samruk-Kazyna JSC;

- Yelzhas Otynshiyev – Representative of Samruk-Kazyna JSC;

- Aidar Ryskulov – Representative of Samruk-Kazyna JSC;

- Meirzhan Yussupov – Chairman of the Management Board of Kazatomprom JSC.

Full biographies of the Company’s Board of Directors and Management Board members are available on the Company's official website www.kazatomprom.kz.

Credit Rating

On 30 October 2023, Moody’s Investors Service reaffirmed Kazatomprom’s credit rating at Baa2, with the outlook changed from stable to positive.

Kazatomprom’s 2023 Third-Quarter and Nine-Months Operational Results1

|

|

Three months ended September 30 |

|

Nine months ended September 30 |

|

||

|

(tU as U3O8 unless noted) |

2023 |

2022 |

Change |

2023 |

2022 |

Change |

|

U3O8 Production volume (100% basis)2 |

5,092 |

5,377 |

-5% |

15,317 |

15,446 |

-1% |

|

U3O8 Production volume (attributable basis)3 |

2,692 |

2,895 |

-7% |

8,102 |

8,309 |

-2% |

|

Group U3O8 sales volume4 |

2,679 |

4,316 |

-38% |

12,206 |

13,332 |

-8% |

|

KAP U3O8 sales volume (incl. in Group)5 |

2,533 |

4,200 |

-40% |

11,098 |

12,232 |

-9% |

|

Group average realized price (USD/lb U3O8)6* |

52.93 |

46.10 |

15% |

48.30 |

42.60 |

13% |

|

KAP average realized price (USD/lb U3O8)7* |

51.90 |

46.08 |

13% |

47.81 |

41.98 |

14% |

|

Average month-end spot price (USD/lb U3O8)8* |

62.63 |

49.13 |

27% |

55.94 |

49.77 |

12% |

Production volumes on both a 100% and attributable basis were slightly lower in the third quarter and for the first nine months of 2023 compared to the same periods of 2022, primarily due to insignificant decrease in the production plan for 2023, compared to 2022, announced at the beginning of the year. Issues associated with limited access to certain key materials, such as sulfuric acid, remain persistent, and might potentially have a negative impact on 2024 production. However, expectations for 2023 production volumes remain unchanged.

In the third quarter and first nine months of 2023, both Group and KAP sales volumes were lower compared to the same periods in 2022, primarily due to the timing of customer-scheduled deliveries. Sales volumes may vary substantially each quarter, and quarterly sales volumes vary year to year due to variable timing of customer delivery requests during the year, and physical delivery activity.

Average realized prices for both the third quarter and first nine months of 2023 were higher compared to the same periods in 2022 due to a higher uranium spot price. The Company’s current overall contract portfolio pricing correlates to uranium spot prices, however deliveries under some long-term contracts in the first nine months of 2023 incorporated a proportion of fixed pricing that was negotiated during a lower price environment. As a result, increases in both the Group and KAP’s average realized prices in the third quarter and first nine months of 2023 were lower than the increases in the spot market price for uranium over the same intervals.

In the uranium market, the trends in quarterly metrics and interim results are rarely representative of annual expectations. For annual expectations, please refer to the updated Company’s uranium sales price sensitivity analysis below, which was adjusted to a wider spot price range.

Uranium sales price sensitivity analysis

The Company will stick to its disclosure practices of preparing and updating uranium sales price analysis table on a semi-annual basis with its half- and full-year Operations and Financial Review. Current additions are introduced amid significant sport market pricing improvements and a resulting growing interest and incoming requests from the investment community.

This sensitivity analysis should be used only as a reference, and actual uranium market spot prices may result in different U3O8 annual average sales prices than those shown in the table. The table is based upon several key assumptions, including estimates of future business opportunities, which may change and are subject to risks and uncertainties outside the Group’s control.

|

Average Annual Spot Price (USD) |

2023E |

2024E |

2025E |

2026E |

2027E |

|

20 |

40 |

25 |

26 |

24 |

25 |

|

40 |

45 |

40 |

39 |

39 |

39 |

|

60 |

51 |

56 |

55 |

57 |

57 |

|

80 |

56 |

70 |

69 |

73 |

73 |

|

100 |

61 |

82 |

81 |

87 |

87 |

|

120 |

66 |

95 |

92 |

101 |

100 |

|

140 |

71 |

108 |

104 |

114 |

114 |

Values are rounded to the nearest dollar. The sensitivity analysis above is based on the following key assumptions:

- Annual inflation is assumed to be 2% in the US for the purposes of this analysis.

- Analysis is as of 30 June 2023 and prepared for 2023–2027 on the basis of minimum average Group annual sales during the specified period of approximately 18 thousand tonnes of uranium in the form of U3O8, of which the volumes contracted as of 30 June 2023 will be sold per existing contract terms (i.e. contracts with hybrid pricing mechanisms with a fixed price component (calculated in accordance with an agreed price formula) and / or combination of separate spot, mid-term and long-term prices); Kazatomprom’s marketing strategy does not target a specific proportion of fixed and market related contracts in its portfolio in order to remain flexible and react appropriately to market signals.

- A difference between sales prices and spot prices is expected for 2023, since deliveries under some long-term contracts in 2023 incorporate a proportion of fixed pricing that was negotiated during a lower price environment.

- For the purpose of the table, uncommitted volumes of U3O8 are assumed to be sold under short-term contracts negotiated directly with the customers and based on spot prices.

Kazatomprom’s 2023 Updated Guidance

|

exchange rate USD / KZT 460 |

Previous 30 June 2023 |

Revised 30 September 2023 |

|

Production volume U3O8 (tU) (100% basis)1 |

20,500 – 21,5002 |

20,500 – 21,5002 |

|

Production volume U3O8 (tU) (attributable basis)3 |

10,600 – 11,2002 |

10,600 – 11,2002 |

|

Group U3O8 sales volume (tU) (consolidated)4 |

17,500 – 18,000 |

18,000 – 18,500 |

|

Incl. KAP U3O8 sales volume (incl. in Group) (tU)5 |

14,500 – 15,000 |

14,650 – 15,150 |

|

Revenue - consolidated (KZT billions)6 |

1,270 – 1,310 |

1,370 – 1,410 |

|

Revenue from Group U3O8 sales, (KZT billions)6 |

1,020 – 1,060 |

1,120 – 1,160 |

|

C1 cash cost (attributable basis) (USD/lb)* |

$13.00 – $14.50 |

$13.00 – $14.50 |

|

All-in sustaining cash cost (attributable C1 + capital cost) (USD/lb)* |

$21.00 – $22.50 |

$20.50 – $22.00 |

|

Total capital expenditures of mining entities (KZT billions) (100% basis)7 |

220 – 230 |

200 – 210 |

As was previously disclosed in Kazatomprom 2Q 2023 Operations and Trading Update, available on the corporate website, www.kazatomprom.kz, all 2023 guidance metrics except for production volumes on both 100% and attributable basis were revised using the updated spot prices estimates and sales portfolio expansion. At this time the Company expects increased sales volume compared to previous guidance indicators due to additional requests from customers to flex up their annual delivery quantities within the frame of existing contracts, as well as some new long-term contracts with the delivery in a prompt window during 2023. Therefore the sales and revenue expectations were revised accordingly.

Revenue, C1 cash cost (attributable basis) and All-in Sustaining cash cost (attributable C1 + capital cost) may vary from the ranges shown, to the extent that the USD / KZT exchange rate and uranium spot price differ significantly from the Company’s assumptions. The change in capital expenditures is due to a shift in the project implementation schedule and savings in procurement of key materials.

Key assumptions used for external metrics, such as exchange rates and uranium prices, are established using third-party sources during the Company’s annual budget process in the previous year or adjustments made due to high volatility in the current year; such assumptions will only be updated on an interim basis in exceptional circumstances.

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Botagoz Muldagaliyeva, Director, Investor Relations

Tel: +7 7172 45 81 80

Email: ir@kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Askar Atagulin, Director, Public Relations

Tel: +7 7172 45 80 63

Email: pr@kazatomprom.kz

A copy of this announcement is available at www.kazatomprom.kz.

About Kazatomprom

Kazatomprom is the world's largest producer of uranium, with the Company’s attributable production representing approximately 22% of global primary uranium production in 2022. The Group benefits from the largest reserve base in the industry and operates, through its subsidiaries, JVs and Associates, 26 deposits grouped into 14 mining assets. All of the Company’s mining operations are located in Kazakhstan and extract uranium using ISR technology with a focus on maintaining industry-leading health, safety and environmental standards (ISO 45001 and ISO 14001 compliant).

Kazatomprom securities are listed on the London Stock Exchange, Astana International Exchange, and Kazakhstan Stock Exchange. As the national atomic company in the Republic of Kazakhstan, the Group's primary customers are operators of nuclear generation capacity, and the principal export markets for the Group's products are China, South and Eastern Asia, Europe and North America. The Group sells uranium and uranium products under long-term contracts, short-term contracts, towards the second shareholders of jointly owned subsidiaries, as well as in the spot market, directly from its headquarters in Astana, Kazakhstan, and through its Switzerland-based trading subsidiary, Trade House KazakAtom AG (THK).

For more information, please see the Company website www.kazatomprom.kz.

Forward-looking statements

All statements other than statements of historical fact included in this communication or document are forward-looking statements. Forward-looking statements give the Company’s current expectations and projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “target”, “believe”, “expect”, “aim”, “intend”, “may”, “anticipate”, “estimate”, “plan”, “project”, “will”, “can have”, “likely”, “should”, “would”, “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future.

THE INFORMATION WITH RESPECT TO ANY PROJECTIONS PRESENTED HEREIN IS BASED ON A NUMBER OF ASSUMPTIONS ABOUT FUTURE EVENTS AND IS SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTY AND OTHER CONTINGENCIES, NONE OF WHICH CAN BE PREDICTED WITH ANY CERTAINTY AND SOME OF WHICH ARE BEYOND THE CONTROL OF THE COMPANY. THERE CAN BE NO ASSURANCES THAT THE PROJECTIONS WILL BE REALISED, AND ACTUAL RESULTS MAY BE HIGHER OR LOWER THAN THOSE INDICATED. NONE OF THE COMPANY NOR ITS SHAREHOLDERS, DIRECTORS, OFFICERS, EMPLOYEES, ADVISORS OR AFFILIATES, OR ANY REPRESENTATIVES OR AFFILIATES OF THE FOREGOING, ASSUMES RESPONSIBILITY FOR THE ACCURACY OF THE PROJECTIONS PRESENTED HEREIN.

The information contained in this communication or document, including but not limited to forward-looking statements, applies only as of the date hereof and is not intended to give any assurances as to future results. The Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to such information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date hereof.