JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the fourth quarter and year ended 31 December 2021.

This update provides a summary of recent developments in the uranium industry, as well as provisional information related to the Company’s key fourth-quarter and 2021 operating and trading results, and 2022 non-financial guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

The 2021 United Nations Climate Change Conference (COP26), held in November 2021 in Glasgow, Scotland, UK, resulted in the adoption of an agreement referred to as the Glasgow Climate Pact. The agreement recognizes the need to take actions through significant, rapid and sustained reductions in global greenhouse gas emissions, including reducing global carbon dioxide emissions by 45% by 2030 relative to 2010 levels, with a further push to net zero emissions around mid-century. In a key outcome of COP26, nations were called upon to accelerate the development, deployment and dissemination of technologies, as well as the adoption of policies, that will drive a transition towards low-emission energy systems, including the rapid scaling-up of clean power generation and enhanced energy efficiency measures.

In another notable development, the European Commission completed a draft of the EU green finance Taxonomy, and began formal consultation with the Platform on Sustainable Finance and the Member States Expert Group on Sustainable Finance, for all Delegated Acts under the Taxonomy Regulation that cover certain gas and nuclear activities. The Commission will analyze the contributions of these groups and formally adopt the complementary Delegated Act in January 2022. It will then be sent to the European Parliament and the European Council, which will have up to six months to review the document. Specific to the nuclear industry in the latest draft, the requirements for nuclear energy’s inclusion into the “green deal” includes the use of "best available technology", reinforced safety and security measures to protect against external hazards, as well as solid waste management and decommissioning provisions. Labeling nuclear as a “climate friendly investment” within the Taxonomy could drive an increase in new builds and life extensions for existing reactors across Europe.

During the fourth quarter, nuclear industry demand-side highlights included:

- Unit 1 of the Shidao-Bay power plant located in the eastern China province of Shandong, was successfully connected to the grid. In what is considered to be the world’s first land-based small modular reactor of modern design, the plant features two high temperature gas-cooled demonstration reactors that drive a single 210 MWe turbine.

- China National Nuclear Corporation (CNNC) reported that Fuqing unit 6, a 1,100 MWe Chinese-designed HPR1000 reactor, located in Fujian province, southeastern China, was connected to the national grid on 01 January 2022.

- CNNC and China Huaneng Group announced that first concrete was poured for the 1,100 MWe HPR1000 PWR at Changjiang unit 4 in Hainan province.

- China General Nuclear Power Group (CGN) announced that construction of its 1,100 MWe HPR1000 PWR at San'ao unit 2 began in December 2021, in Zhejiang Province. With the start of construction of San'ao unit 2, CGN now has seven nuclear power units under construction with total installed capacity of 8.3 GWe.

- EDF Energy’s Hunterston B unit 3 nuclear plant in Scotland, UK, was permanently shut down in November 2021, followed by the permanent closure of unit 4 in January 2022. The two Hunterston B advanced gas-cooled reactors came online in February 1976 and were initially expected to run for 25 years, but each had their generating lifespan increased to more than 45 years.

- Three nuclear power plants were disconnected from Germany’s grid on 31 December 2021, under the country’s nuclear phase-out policy. The shutdowns included PreussenElektra’s 1,480 MWe Brokdorf reactor (PWR) in the northern state of Schleswig-Holstein, the 1,430 MWe Grohnde reactor (PWR) in Lower Saxony, and RWE’s 1,300 MWe Gundremmingen C (BWR) in Bavaria.

- Rosenergoatom’s Kursk unit 1 (RBMK-1000) in Kurchatov, Kursk region, Russia, was permanently shut down after 45 years of operation. According to Alexander Uvakin, acting director of the power plant, the unit safely generated more than 251 billion kilowatt hours of electricity over its lifespan.

- Rosatom announced that first concrete was poured to begin construction of a VVER-1000 reactor at Kudankulam unit 6, located in the state of Tamil Nadu, India.

- Armenia extended the life of the 376 MWe Metsamor unit 2 (VVER) to 2026 as a result of work on replacement and modernisation of equipment, which was performed in collaboration with Rosatom.

Several “unconventional demand” developments emerged during the fourth quarter:

- "ANU Energy OEIC Ltd." was established, a physical uranium fund with a US$50 million total seed investment from the fund’s founders: Kazatomprom (48.5%), National Investment Corporation of the National Bank of Kazakhstan JSC (48.5%) and Genchi Global Limited (3%). The Fund intends to store physical uranium as a long-term investment.

- Sprott Physical Uranium Trust increased the value of its at-the-market offering, with approval to issue up to a value of US$3.5 billion in trust units.

- In a similar development, Yellow Cake Plc. announced its successful equity fundraise to purchase physical uranium amounting to about 3 million pounds U3O8.

On the supply side, Russian uranium producer JSC Atomredmetzoloto (ARMZ) reported that its subsidiary, JSC Dalur, began construction of a pilot site for in-situ recovery mining of the Dobrovolnoye uranium deposit in the Kurgan region of Russia. ARMZ also reported that JSC Khiagda is preparing for development of its Kolichikan uranium deposit in Russia's Republic of Buryatia, with drilling operations and construction projects underway.

Also impacting future supply, the Ministry of Energy of the Republic of Kazakhstan approved an amendment for the right to commence commercial production at JV Budenovskoye’s Budenovskoye Blocks 6 and 7, with a commercial ramp-up of up to 2,500 tU beginning no earlier than 2024 (Please see Company Developments for more information).

Further down the nuclear fuel supply chain, Kazakhstan launched the Ulba Fuel Assembly plant in November. The fuel assembly facility has a capacity of 200 tons of uranium as fuel bundles per year. The technology from French company Framatome was used for the Ulba-FA plant, and the new facility will be using the existing fuel pellet manufacturing capabilities of the Ulba Metallurgical Plant (UMP). Ulba-FA LLP is a Kazakhstani and Chinese joint venture with UMP JSC (a subsidiary of NAC Kazatomprom JSC) holding a 51% interest, and CGNPC-URC (a subsidiary of China General Nuclear Power Corporation), holding a 49% interest.

Market Pricing and Activity

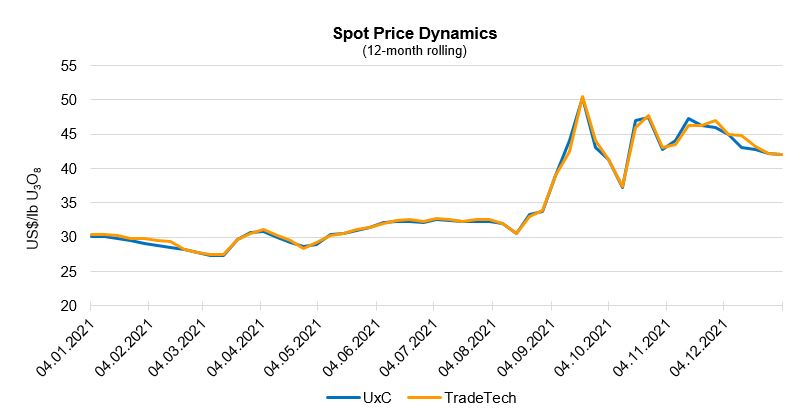

Spot market activity in the fourth quarter fell compared to the third quarter, though it remained higher than the historical average. During the quarter, the spot price was highly volatile, initially declining to US$37.35 per pound U3O8 in October, before rising sharply to US$47.00 due to increased activity led primarily by financial participants. In November, the spot price slid to about US$43.00 before finding strength and rising to US$46.50 at the end of the month. In December, spot market activity slowed down substantially, leading to a gradual price decline to US$42.00 per pound U3O8. According to third-party market data, spot volumes transacted through 2021 were about 25% higher than last year. A total of 97 million pounds U3O8 (37,300 tU) was transacted at an average weekly spot price of US$35.05 per pound, compared to 77 million pounds U3O8 (29,600 tU) at an average weekly spot price of US$29.60 per pound in 2020.In the term market, third-party data indicated that contracted volumes totalled about 72 million pounds U3O8 (27,700 tU) through 2021, compared to about 53 million pounds U3O8 (20,400 tU) in 2020. The 36% increase in term market activity, resulted in an increase of the average long-term price by about US$8.00 per pound U3O8 year-over-year, to US$42.75 (reported only on a monthly basis by third-party sources).

Company Developments

Corporate Update

At the very beginning of 2022, subsequent to the end of the quarter, a state of emergency was declared following civil protests related to a significant increase in the cost of liquefied petroleum gas, that began in the western town of Zhanaozen, Mangystau region, Kazakhstan,. The protests spread to major centers, leading to serious unrest in Almaty. A state of emergency order was in effect until 19 January 2022 and included a curfew and a ban on mass gatherings. The Kazakh Government resigned on 05 January 2022 and a new government was appointed and functional as of 11 January 2022. The large-scale anti-terrorism operations which included both Kazakh police, security and military forces, as well as support from the regional Collective Security Treaty Organization (CSTO), has since been concluded. As of 19 January, the situation throughout the country stabilized, the state of emergency was lifted, and the withdrawal of units of the CSTO forces from Kazakhstan was completed.

Kazatomprom’s focus remains on business continuity, including the safety and security of its employees and operations and as previously disclosed, the Company’s production facilities were not impacted and are operating normally. Kazatomprom’s risk management and business continuity plans proved to be robust, with no delays or disruptions to the Company’s uranium production, deliveries or sales plans. At no point were CSTO forces deployed to the vicinity of Kazatomprom’s infrastructure or operations.

COVID-19 Update

With Omicron-variant COVID-19 cases rising since the beginning of 2022 and forcing red-zone centres, including Nur-Sultan, Almaty and Shymkent back into severe government-mandated restrictions, the Company continues to rigorously monitor the COVID-19 situation to ensure current protocols remain effective. Existing protocols have been reinforced to minimize the spread by introducing PCR testing for anyone accessing the mine sites. Health-related pandemic risks have remained well mitigated within the Company and if a case of COVID-19 is detected, proactive and preventive measures are implemented to contain the spread, with the health of the individual being constantly monitored and medical assistance provided as necessary.

Vaccination status is being monitored on a daily basis: to date, each of the Group’s uranium mining entities has surpassed the 90% level of full immunization coverage, with several sites now 100% fully vaccinated. Taken as a whole, including the corporate headquarters and all Group entities, as of 24 January 2022, 94% (18,035) of employees are partially vaccinated, with 93% fully vaccinated.

JV Budenovskoye Commercial Production Contract Update

As previously disclosed in November 2021, the Company’s Board of Directors approved a Life of Mine plan that JV Budenovskoye LLP (“JV Budenovskoye” or “the JV”) submitted to the Ministry of Energy of the Republic of Kazakhstan. On 21 December 2021, the related amendment for the right to commence commercial production under JV Budenovskoye’s Subsoil Use Agreement, was signed. The 25-year plan (2021 – 2045) provides for the future development of Budenovskoye Blocks 6 and 7 after the completion of its ongoing pilot production program, with a commercial ramp-up of up to 2,500 tU beginning no earlier than 2024, and the potential for maximum annual production capacity of up to 6,000 tU no earlier than 2026. The timing of commissioning plans and future production rates remain subject to annual review and may be adjusted based on Kazatomprom’s strategy and an ongoing assessment of market conditions.

Under an agreement signed by the JV partners, the JV’s anticipated rampup production from 2024 – 2026 is fully committed for supplying the Russian civil nuclear energy industry, under an offtake contract at market-related terms. Established in 2016, JV Budenovskoye is owned 51% by Kazatomprom and 49% by Stepnogorsk Mining and Chemical Plant LLP (“SMCC”).

JV Ortalyk Commercial Production Contract

On 14 December 2021, the Subsoil Use Agreement for the right to commence commercial production from the Zhalpak deposit was signed between the Kazakh Ministry of Energy and Kazatomprom. As per the agreements related to the sale of a 49% share of Ortalyk LLP to CGN Mining UK Limited (a CGNPC subsidiary) that were finalized in July 2021, on 28 December 2021, the right to commence commercial production from Zhalpak was transferred to JV Ortalyk LLP. The 21-year plan (2022 – 2042) provides for development of the Zhalpak mine according to the JV Ortalyk mine plan, with a maximum annual production capacity of up to 900 tU no earlier than 2030.

Board of Directors Change

On 11 January 2022, Mr. Bolat Akchulakov, a Kazatomprom Board member representing the interests of majority shareholder Samruk-Kazyna, was appointed Minister of Energy and has therefore resigned from his position on Kazatomprom’s Board of Directors.

Samruk Kazyna Organizational Changes

On 24 January 2022, majority shareholder Samruk-Kazyna (“the Fund”) announced the approval of a new organizational structure. According to the new structure, the total number of employees within the Fund was reduced from 248 to 124, with senior management positions reduced from 10 to 5, and the number of structural units decreasing from 27 to 18. The Fund also decided to close all offices abroad. There have been no changes related to Samruk-Kazyna’s ownership status in Kazatomprom.

In addition to its own restructuring plans, Samruk-Kazyna recommended that all of its portfolio companies reduce the number of administrative employees by 50% and release all managers responsible for procurement. As a publicly traded company, Kazatomprom will continue to maintain high standards and best practices for corporate governance, and any organizational changes and/or dismissals for any reason would only be considered in strict compliance with the local labor code, laws and internal policy documents. Any decision on changes to the Company’s headcount and organizational structure are subject to approval by Kazatomprom’s Board of Directors following an internal evaluation.

Kazatomprom’s 2021 Fourth-Quarter Operational Results1

|

|

Three months ended December 31 |

|

Year ended December 31 |

|

||

|

(tU as U3O8 unless noted) |

2021 |

2020 |

Change |

2021 |

2020 |

Change |

|

Production volume (100% basis)2 |

5,859 |

4,386 |

34% |

21,819 |

19,477 |

12% |

|

Production volume (attributable basis)3 |

3,066 |

2,427 |

26% |

11,858 |

10,736 |

10% |

|

Group sales volume4 |

8,117 |

6,575 |

23% |

16,526 |

16,432 |

1% |

|

KAP sales volume (incl. in Group)5 |

6,788 |

5,402 |

26% |

13,586 |

14,126 |

-4% |

|

KAP average realized price (USD/lb U3O8)6* |

34.49 |

29.31 |

18% |

32.36 |

29.63 |

9% |

|

Average month-end spot price (USD/lb U3O8)7* |

44.33 |

29.86 |

48% |

35.28 |

29.96 |

18% |

1 All values are preliminary.

2 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it therefore disregards the fact that some portion of that production may be attributable to the Group’s joint venture partners or other third party shareholders. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, which corresponds only to the size of such interest; it therefore excludes the remaining portion attributable to the JV partners or other third party shareholders, except for production from JV “Inkai” LLP, where the annual share of production in 2021 as per the terms of Implementation Agreement as disclosed in IPO Prospectus, amounted 1,400 tU.

4 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity). Volume does not include approximately 225 tU equivalent sold as UF6 in 4Q21.

5 KAP sales volume (incl. in Group): includes only the total external sales of KAP HQ and Trade House KazakAtom AG (THK). Intercompany transactions between KAP HQ and THK are not included. Volume does not include approximately 225 tU equivalent sold as UF6 in 4Q21.

6 KAP average realized price: the weighted average price per pound for the total external sales of KAP HQ and THK. The pricing of intercompany transactions between KAP HQ and THK are not included.

7 Source: UxC LLC, TradeTech. Values provided are the average of the month-end uranium spot prices quoted by UxC and TradeTech, and not the average of each weekly quoted spot price throughout the month. Contract price terms generally refer to a month-end price.

* Note the conversion of kgU to pounds U3O8 is 2.5998.

Production on both a 100% and attributable basis was higher for 2021 compared to 2020, and notably higher for the fourth quarter of 2021 compared to the same period in 2020. The pandemic-related safety measures that were implemented in 2020 impacted production volumes throughout the second half of that year – production in 2020 should therefore be considered exceptionally low, while 2021 represents a production level that is approximately 20% below subsoil use agreement volumes.

Uranium sales at the Group level in 2021 were in line with 2020. Due to the timing of customer requirements and differences in the timing of deliveries, a larger proportion of both Group and KAP sales occurred in the fourth quarter, resulting in higher sales in the final quarter of 2021 compared to the same period in 2020. KAP sales volume was modestly lower in 2021 compared to 2020 due to additional sales by consolidated subsidiaries to JV partners.

Higher uranium prices in 2021 had a positive impact on Kazatomprom’s average realized price compared to 2020. However, due to the increased volatility of uranium prices during 2021, KAP’s average realized price for fourth quarter and the year was lower than the corresponding average month-end uranium spot price, and during the fourth quarter many deliveries took place based on pricing that was locked-in in various ways at an earlier date.

Kazatomprom’s 2022 Production and Sales Guidance

|

2021 |

2022 |

|

|

Production volume U3O8 (tU) (100% basis) 1 |

21,700 – 22,000 |

21,000 – 22,000 |

|

Production volume U3O8 (tU) (attributable basis) 2 |

11,800 – 12,000 |

10,900 – 11,500 |

|

Group sales volume (tU) (consolidated) 3 |

16,300 – 16,800 |

16,300 – 16,800 |

|

KAP sales volume (tU) (incl. in Group) 4 |

13,500 – 14,000 |

13,400 – 13,900 |

1 Production volume U3O8 (tU) (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it disregards that some portion of production may be attributable to the Group’s JV partners or other third-party shareholders.

2 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, corresponding only to the size of such interest; it excludes the portion attributable to the JV partners or other third-party shareholders, except for JV “Inkai” LLP, where the annual share of production is determined as per Implementation Agreement as disclosed in IPO Prospectus. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity).

4 KAP sales volume: includes only the total external sales of KAP and THK. Intercompany transactions between KAP and THK are not included

* Note that the conversion of kgU to pounds U3O8 is 2.5998.

Kazatomprom’s production expectations for 2022 remain consistent with its market-centric strategy and the intention to flex down planned production volumes by 20% for 2018 through 2023 (versus planned production levels under Subsoil Use Agreements). Production volume in 2022 is expected to be between 21,000 tU and 22,000 tU on a 100% basis, similar to 2021 at the top end of the range. However, pandemic-related supply chain challenges have continued to result in limited access to certain key operating materials and equipment (production reagents, certain types of pipes and pumps, specialized equipment, drilling rigs), which had a material impact on the Company’s wellfield development and production schedules in 2021, adding additional risk to production in 2022 and resulting in a wider range for the expected production volume. On an attributable basis, 2022 production volume is expected to be between 10,900 tU to 11,500 tU, which is lower than 2021 primarily due to the sale of a 49% share of Ortalyk LLP to CGN Mining UK Limited in mid-2021, as well as the above-mentioned supply chain risks.

Sales volume guidance for 2022 is also aligned with the Company’s market-centric strategy. The Group expects to sell between 16,300 tU and 16,800 tU, which includes KAP sales of between 13,400 tU and 13,900 tU, in line with sales volumes in 2021.

The Company continues to target an ongoing inventory level of approximately six to seven months of annual attributable production. However, inventory could fall below this level in 2022 due to pandemic-related supply chain challenges and production losses. As such, during the fourth quarter of 2021, several transactions to purchase uranium in the spot market were carried out and the Company will continue to monitor market conditions for opportunities to optimize its inventory.

Wellfield development, procurement and supply chain issues, including inflationary pressure on production materials and reagents, are expected to continue throughout 2022, impacting the Company’s financial metrics. In addition, the Company’s costs could be impacted by potential changes to the tax code in Kazakhstan and by possible local social funding requests, although these risks cannot be quantified or estimated at this time. Financial guidance for 2022 will be published in the 2021 Operating and Financial Review, expected to be released on 17 March 2022.

Conference Call Notification - 2021 Operating and Financial Review (17 March 2022)

Kazatomprom expects to schedule a conference call to discuss the full 2021 operating and financial results, after they are released on Thursday, 17 March 2022. Further details will be provided closer to the date of the event.

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Cory Kos, Director of Investor Relations

Tel: +7 (8) 7172 45 81 80

Email: ir@kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Torgyn Mukayeva, Chief Expert of GR & PR Department

Tel: +7 (8) 7172 45 80 63

Email: pr@kazatomprom.kz

About Kazatomprom

Kazatomprom is the world's largest producer of uranium, with the Company’s attributable production representing approximately 23% of global primary uranium production in 2020. The Group benefits from the largest reserve base in the industry and operates, through its subsidiaries, JVs and Associates, 26 deposits grouped into 14 mining assets. All of the Company’s mining operations are located in Kazakhstan and extract uranium using ISR technology with a focus on maintaining industry-leading health, safety and environment standards.

Kazatomprom securities are listed on the London Stock Exchange, Astana International Exchange, and Kazakhstan Stock Exchange. As the national atomic company in the Republic of Kazakhstan, the Group's primary customers are operators of nuclear generation capacity, and the principal export markets for the Group's products are China, South and Eastern Asia, Europe and North America. The Group sells uranium and uranium products under long-term contracts, short-term contracts, as well as in the spot market, directly from its headquarters in Nur-Sultan, Kazakhstan, and through its Switzerland-based trading subsidiary, Trade House KazakAtom AG (THK).

For more information, please see the Company website at http://www.kazatomprom.kz

Forward-looking statements

All statements other than statements of historical fact included in this communication or document are forward-looking statements. Forward-looking statements give the Company’s current expectations and projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plan,” “project,” “will,” “can have,” “likely,” “should,” “would,” “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future. THE INFORMATION WITH RESPECT TO ANY PROJECTIONS PRESENTED HEREIN IS BASED ON A NUMBER OF ASSUMPTIONS ABOUT FUTURE EVENTS AND IS SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTY AND OTHER CONTINGENCIES, NONE OF WHICH CAN BE PREDICTED WITH ANY CERTAINTY AND SOME OF WHICH ARE BEYOND THE CONTROL OF THE COMPANY. THERE CAN BE NO ASSURANCES THAT THE PROJECTIONS WILL BE REALISED, AND ACTUAL RESULTS MAY BE HIGHER OR LOWER THAN THOSE INDICATED. NONE OF THE COMPANY NOR ITS SHAREHOLDERS, DIRECTORS, OFFICERS, EMPLOYEES, ADVISORS OR AFFILIATES, OR ANY REPRESENTATIVES OR AFFILIATES OF THE FOREGOING, ASSUMES RESPONSIBILITY FOR THE ACCURACY OF THE PROJECTIONS PRESENTED HEREIN. The information contained in this communication or document, including but not limited to forward-looking statements, applies only as of the date hereof and is not intended to give any assurances as to future results. The Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to such information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date hereof.